Innovative, Objective, Practical

Date: July 20, 2025

In the first half of 2025, China faced growing external turbulence alongside interwoven domestic challenges. Despite these pressures, the economy demonstrated overall stability and continued progress in high-quality development. Tariff tensions eased following May’s negotiations in Switzerland, reducing potential impacts on export sectors. Coupled with domestic policy support, economic activity showed signs of recovery, though challenges persisted. Moving forward, policy implementation acceleration is needed to enhance multiplier effects, while domestic demand to be expanded by leveraging people’s aspirations for a better life.

The Economy Operated with Overall Stability.

In H1 2025, GDP grew 5.3% y/y at constant prices, 5.4% in Q1 and 5.2% in Q2. Value-added output rose across primary, secondary, and tertiary industries in Q2. Service industry remained a key growth engine, expanding 5.5% y/y in H1, with information transmission, software, and IT services leading at 11.1% growth. June’s Manufacturing Production Index and New Orders Index both increased m/m, signaling accelerated output and improved demand.

Tariff Tensions Disrupted Export Trends.

H1 goods exports rose 7.2% y/y in RMB terms, up 0.3 pp from Q1 and exceeding 2024’s performance, mostly due to 2024’s low base and tariff war effects. Following May’s Sino-U.S. tariff reductions, the y/y decline in U.S.-bound exports narrowed from -34.5% in May to -16.1% in June. Meanwhile, China maintained robust export growth to re-export hubs in June. Exports to ASEAN and Hong Kong SAR accelerated m/m. With pent-up U.S. orders fulfilled and given increased scrutiny of re-exports in U.S. trade agreements, future exports could face pressure.

Industrial Output Growth Accelerated Y/Y.

H1 industrial value-added for enterprises above the designated size rose 6.4% y/y, 0.6 pp higher than full-year 2024. Q1 and Q2 saw 6.5% and 6.3% growth respectively. Key drivers included: expanded large-scale equipment upgrade and consumer goods trade-in programs releasing domestic demand; and digital, smart and green transition in industrial development, notably digital product manufacturing went up 9.9% y/y, outpacing industrial averages for 23 straight months.

Investment Growth Decelerated Y/Y.

H1 fixed-asset investment grew 2.8% y/y, down 0.9 pp Jan–May. By sector, infrastructure went up 4.6% y/y (down 1.0 pp Jan–May), manufacturing up 7.5% y/y (down 1.0 pp Jan–May), real estate down 11.2% y/y (down 0.5 pp Jan–May) reflecting persistent stabilization pressures. While large-scale equipment upgrade and consumer goods trade-in programs continued to drive strong growth in high-end, smart, and green manufacturing, investment growth slowed post-acceleration across all three sectors.

Trade-in Policy Accelerates Consumption.

Driven by a series of policies aimed at promoting consumption, domestic demand continued to increase. H1 retail sales rose 5.0% y/y, up 0.4 pp from Q1 and continuing quarterly acceleration since Q3 2024. June sales grew 4.8% y/y, down 1.6 pp m/m. The implementation and optimization of consumer goods trade-in program boosted goods and services consumption, demonstrating strong momentum. H1 service retail picked up pace and rose 5.3% y/y, up 0.3 pp compared to Q1. Policy sustainability and consumption impacts warrant monitoring.

Pushing Prices Toward Higher Levels.

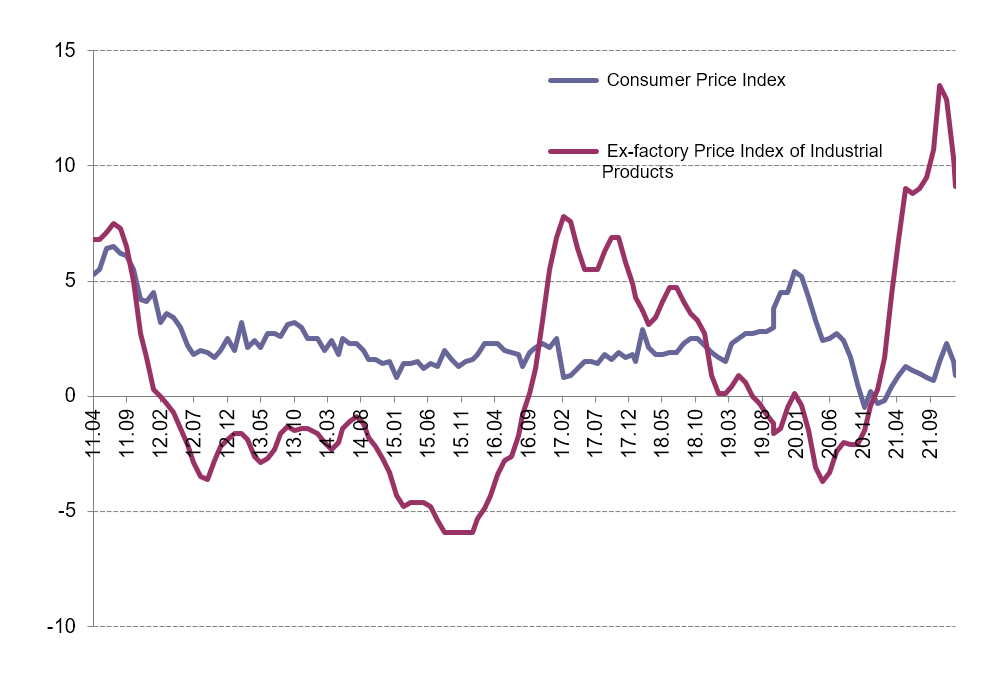

H1 CPI averaged -0.1% y/y, unchanged from Q1. Monthly volatility stemmed from Chinese New Year timing seen in CPI increased 0.5% in January, then decreased 0.7% in February. March–May CPI decline narrowed to -0.1%, before turning positive in June (up 0.1% y/y) due to international commodity price fluctuations and domestic consumer demand stimulus policies. The narrowing decline in food prices and the expanding growth in service prices are the main contributors to Q2’s improvement. H1 PPI fell 2.8% y/y, continuing its downward trend pressured by seasonal drops in prices across certain domestic raw material manufacturing industries, lower energy prices driven by increased solar, wind and hydropower generation, and price pressures faced by some export-led sectors.

Image source: IE Insights (2022). https://www.ie.edu/insights/articles/our-urban-life-in-2022/

Date: March 20, 2025

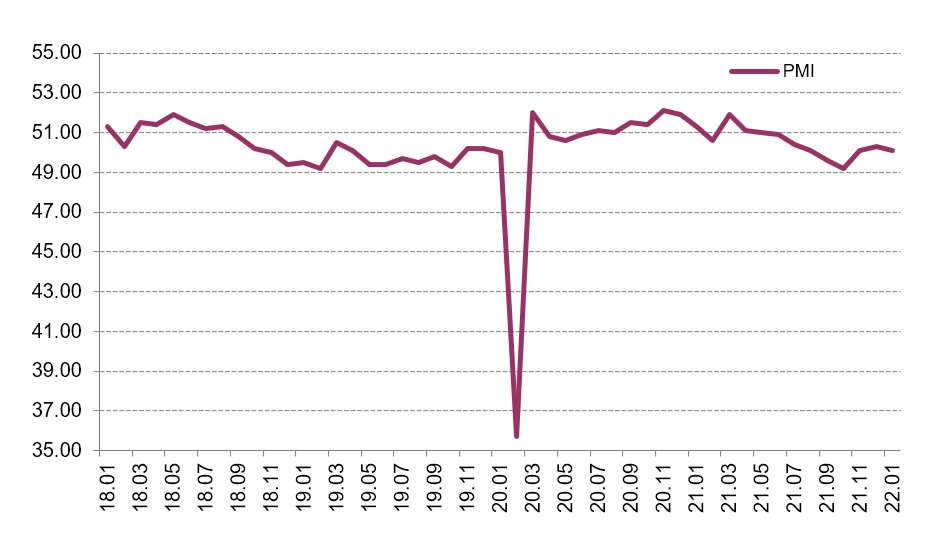

Following the Spring Festival, economy regained momentum in February as businesses resumed operations, accelerating production and commercial activity. Key indicators such as the Manufacturing Purchasing Managers’ Index (PMI), Non-Manufacturing Business Activity Index, and Composite PMI Output Index all rebounded month-on-month, remaining in expansionary territory. While these figures signal a tentative recovery from earlier lows, sustaining growth will demand stronger policy reinforcement and expedited implementation.

Economic Recovery Shows Marginal Improvement from Low Levels

In February, the Composite PMI Output Index rose by 1.0 percentage points from the previous month to 51.1%, returning to expansion territory. The Manufacturing PMI, up 1.1 percentage points to 50.2%, emerged as the primary growth driver. A breakdown of the index shows that both production and demand within the manufacturing sector improved, with the Production Index and New Orders Index rising by 2.7 and 1.9 percentage points, respectively, to 52.5% and 51.1%. Both indices entered expansion territory, indicating a notable improvement in manufacturing supply and demand. This resurgence bolstered corporate confidence, pushing the Purchasing Volume Index up by 2.9 percentage points to 52.1%. On the non-manufacturing side, the Non-Manufacturing Business Activity Index edged up 0.2 percentage points to 50.4% in February.

Export Disruptions Due to Tariffs and "Front-Loading"

From January to February, Merchandise exports grew 3.4% year-on-year, though this was a slight moderation compared to full-year 2024 and December figures. Trade with the U.S. expanded at a slower pace, with exports rising 2.9% year-on-year—5.1 percentage points lower than in December 2024—partly reflecting adjustments to U.S. tariff hikes. Meanwhile, shipments of products that retain a competitive edge under current tariff conditions, such as smartphones and laptops, saw a boost, possibly as exporters sought to stay ahead of potential U.S. trade restrictions. However, taking into account two fewer working days in January-February 2025 compared to the same period in 2024, the year-on-year export growth rate would have been higher if measured on a per-working-day basis.

New Growth Drivers Accelerate Industrial Expansion

Industrial output from large-scale enterprises grew 5.9% year-on-year in January-February, extending the robust momentum seen since Q4 2024. The pace edged up 0.2 and 0.1 percentage points from the fourth quarter and full year of 2024, respectively. Externally, export momentum sustained industrial expansion, with export delivery values rising 6.2% year-on-year—1.1 percentage points faster than 2024’s annual rate. Domestically, policies such as large-scale equipment upgrades and consumer trade-in programs, expanded in 2025, spurred industrial modernization and unlocked consumption potential, further driving growth. On the supply side, equipment manufacturing and high-tech industries led the charge, with rapid growth continuing to optimize the industrial structure.

"Two Major" Projects Fuel Investment Growth

In January and February, investment increased by 4.1% year-on-year, up by 0.9 percentage points compared to the whole of last year. First, support for "Two Major" projects (advancing national strategic initiatives and enhancing key security capabilities) has strengthened, with physical work volumes picking up, driving a faster growth in infrastructure investment. Infrastructure investment rose by 5.6% year-on-year in January and February, accelerating by 1.2 percentage points from 2024, contributing 1.1 percentage points to overall investment growth. The "Two New" policies (promoting large-scale equipment upgrades and consumer goods trade-ins) have been further expanded, with their effects becoming increasingly evident, spurring rapid growth in equipment investment. Second, progress in the high-quality development of key industrial chains is solid, with the transformation of traditional industries accelerating, leading to strong growth in manufacturing investment. Third, real estate policies have mitigated the decline in investment, showing early signs of stabilization.

Trade-In Programs and Green Consumption Boost Retail Sales

In January and February, retail sales grew by 4.0% year-on-year, with goods retail increasing by 3.9% and catering revenue rising by 4.3%. The growth in consumer spending was driven by the expansion of trade-in policies, which quickly unlocked demand for appliances and electronics. Meanwhile, the increasing focus on green and health-conscious products fueled strong growth in the eco-friendly and wellness sectors. Additionally, a surge in travel and leisure activities led to a rapid increase in spending on transportation, accommodation, and related services, highlighting a broader recovery in consumption.

Efforts Needed to Stimulate a Balanced Price Recovery

In February, China’s Consumer Price Index (CPI) fell 0.2% month-on-month and 0.7% year-on-year, reflecting the combined impact of Chinese New Year timing, holiday effects, and volatile global commodity prices. The year-on-year decline was primarily driven by a high base effect: food and service prices surged during February 2024’s holiday period, inflating the comparison base and putting downward pressure on this year’s figure. Food prices dropped 3.3% year-on-year, accounting for over 80% of the CPI decline (contributing 0.6 percentage points to the total 0.7% drop). This sharp contraction in food costs—the largest drag on prices—tipped the CPI into deflationary territory. Meanwhile, the Producer Price Index (PPI) continued to decline due to seasonal industrial sluggishness and softer global commodity prices. However, both month-on-month and year-on-year PPI decreases narrowed by 0.1 percentage points, signaling easing deflationary pressures.

Date: Feb 20, 2025

In January, due to the Spring Festival holiday and seasonal factors, industrial production entered an off-season, with the Producer Price Index (PPI) declining month-on-month. However, service and food prices rose significantly affected by the timing of the holiday, along with a rebound in gasoline prices, collectively driving an expansion in the Consumer Price Index (CPI) year-on-year growth. Overall, despite signs of moderation, economic activity remains on a positive trajectory, underscoring the need to expedite the implementation of supportive measures

Economic Growth Moderates, but Certain Sectors Gain Momentum

In January, the Composite Purchasing Managers’ Index fell by 2.1 percentage points month-on-month to 50.1%, reflecting impacts from the Spring Festival holiday and the return of employees to their hometowns. This indicates a broad-based slowdown, though overall economic expansion persists. Driven by the Spring Festival effect, sectors related to residents' travel and consumption—such as road transportation, accommodation, catering, ecological protection, and public facility management—saw their Business Activity Indexes rebound into expansionary territory, signaling greater market vitality. Meanwhile, sectors including air transport, postal services, telecommunications, broadcasting, satellite transmission, and monetary financial services maintained robust Business Activity Indexes above 55.0%, sustaining rapid growth in output.

Surge in Aggregate Social Financing

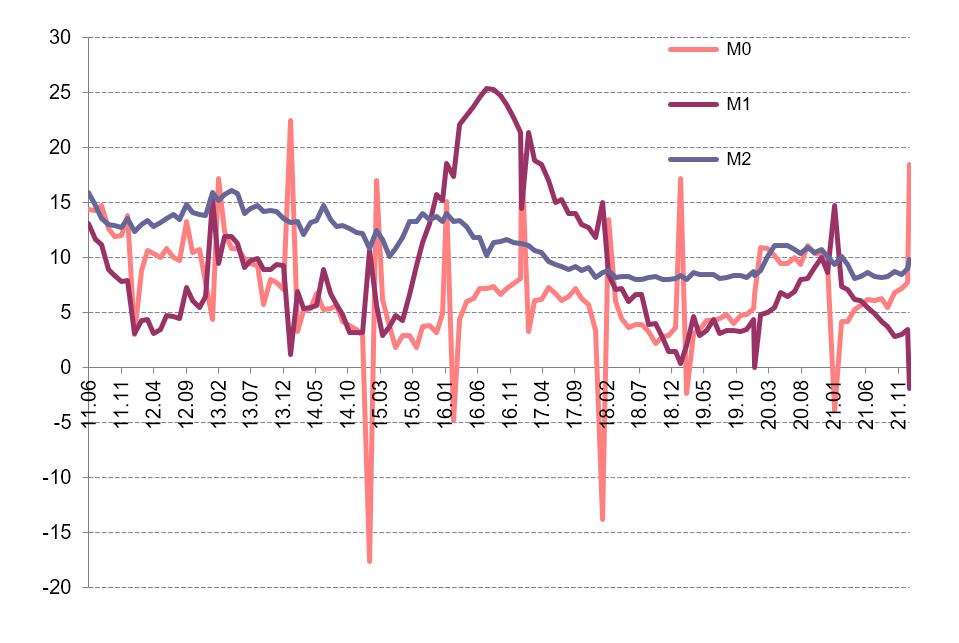

In January, total social financing increased by 7.06 trillion yuan, up by 586.6 billion yuan compared to the same period last year. Financial institutions issued 5.13 trillion yuan in new RMB loans (including loans to non-bank financial institutions), a year-on-year increase of 210 billion yuan. Structurally, the surge was driven by government bonds and corporate financing, while household borrowing remained weak. Corporate financing hit record highs, with medium- and long-term loans growing further despite a high base. The demand for household short-term loans remained low, likely due to the timing of the Spring Festival. Additionally, the reduced demand for business loans to refinance existing mortgages, following cuts in mortgage rates, weighed on medium- to long-term business loans.

Property Market Prices See Divergent Trends

In January, housing prices in first-tier cities continued to rise month-on-month, whereas second- and third-tier cities saw slight declines, reflecting a clear divergence in trends. Specifically, new home prices in first-tier cities increased by 0.1% month-on-month, though the rate of growth slowed by 0.1 percentage point compared to December. In second-tier cities, new home prices rose by 0.1%, marking the first increase since June 2023, while third-tier cities saw a 0.2% decline. For existing homes, first-tier prices edged up by 0.1%, a 0.2 percentage point slowdown from December, second-tier prices dropped by 0.3%, and third-tier prices fell by 0.4%. Year-on-year, price declines narrowed across all city tiers, suggesting gradual stabilization.

Core Consumption Recovery Emerges as Economic Stabilizer

In January, industrial production remained subdued due to the holiday, with the PPI falling by 0.2% month-on-month and 2.3% year-on-year—unchanged from the previous month's annual decline. Prices in non-ferrous metal mining and processing saw significant increases, while ferrous metal smelting, coal mining, and related industries accounted for nearly 90% of the PPI’s annual decline, contributing 2.11 percentage points. The CPI, however, expanded year-on-year, fueled by holiday-driven service and food price surges along with higher gasoline prices. Notably, the core CPI (excluding food and energy) rose for the fourth consecutive month, climbing 0.5% month-on-month and 0.6% year-on-year, with both growth rates accelerating from December.

Date: Jan 20, 2025

Despite external pressures and domestic challenges, China's economy exhibited stability and steady progress in 2024. Targeted incremental policies boosted confidence and facilitated a strong recovery. Export growth decelerated in the first three quarters owing to diminished global demand, although industrial supply chains remained resilient. In Q4, an increase in "front-loading exports" stimulated manufacturing growth, whereas large-scale equipment upgrades and consumer goods trade-in programs maintained ongoing demand and investment in manufacturing. Existing policies, together with new stimulus measures, have spurred local infrastructure investment, though further improvements are required. The recovery in the real estate sector remains sluggish, and its economic contribution has not yet improved.

Overall Economic Stability with Continued Growth.

In 2024, China’s GDP increased by 5.0% at constant prices, with quarterly growth rates of 5.3% in Q1, 4.7% in Q2, 4.6% in Q3, and 5.4% in Q4, indicating a stable upward trend. From Q4 onwards, sustained policy impacts significantly enhanced market expectations and confidence, resulting in positive shifts in both the capital and real estate markets. The service sector grew by 5.8% year-on-year in Q4, an increase of 1.0 percentage point from Q3. The stock market surged, with trading volumes in the Shanghai and Shenzhen markets rising by 126.4% and 124.4% year-on-year respectively, significantly outperforming the first three quarters.

Exports See Consistent Growth.

In 2024, China’s goods exports increased by 7.1%, indicating a rise of 6.5 percentage points from the previous year, significantly contributing to economic growth. In Q4, "front-loading exports" surged, and strong consumption demand in Europe and the U.S. stimulated a resurgence in export growth. In December, exports rose 10.9% year-on-year, representing an increase of 4.0 percentage points from the previous month. The U.S. remained the primary driver of growth, whereas exports to ASEAN increased by 18.9%. Products sensitive to U.S. tariffs, such as automobiles, machinery, auto parts, and textile yarns, saw notable growth. Furthermore, Chinese industrial goods gained global competitiveness, further accelerating export growth.

Manufacturing Fuels Industry Resilience.

In 2024, China’s large-scale industrial enterprises exhibited stable growth, with value-added industrial output rising by 5.8% year-on-year, reflecting a 1.2 percentage point acceleration from the previous year. Manufacturing played a central role, rising by 6.1%, whereas mining and utilities grew by 3.1% and 5.3%, respectively. Policy support continued to advance the manufacturing sector toward higher-end development, with equipment manufacturing increasing by 7.7% and high-tech manufacturing by 8.9%, both exceeding overall industrial growth.

Investment Growth Accelerates with Policy Support.

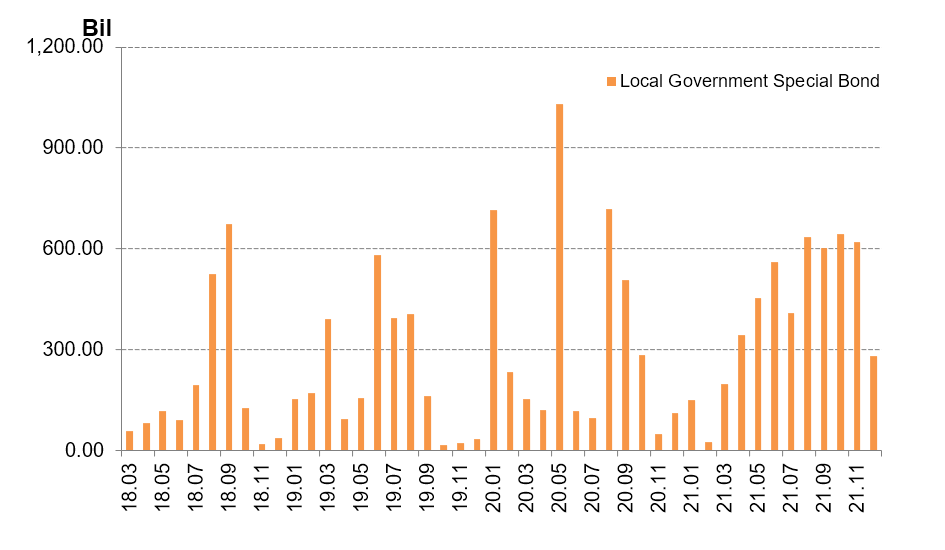

Fixed asset investment increased by 3.2% in 2024, up 0.2 percentage points over the previous year. Backed by ultra-long-term special government bonds and local government special bonds, major infrastructure projects advanced rapidly, boosting infrastructure investment by 4.4%. Manufacturing investment increased by 9.2%, indicating the sector’s shift toward high-end and advanced industries. Investment in high-tech manufacturing and services grew by 7.0% and 10.2%, respectively. In Q4, targeted policy measures contributed to the stabilization of the real estate market, easing the decline in new home sales and driving the growth in the real estate production index for three consecutive months.

Consumption Growth Requires Further Stimulus.

In 2024, retail sales of consumer goods increased by 3.5%, accelerating in Q3 and Q4, but still below the previous year’s pace. Retail sales of goods rose by 3.2%, whereas dining revenue increased by 5.3%, both below the previous year’s growth rates. Sales at large brick-and-mortar retailers rose by 1.9%, with new retail formats performing well. Policies promoting trade-ins for consumer goods resulted in stronger sales in key categories, including home appliances and audiovisual equipment, which maintained double-digit growth for four consecutive months. Auto and furniture sales returned to positive growth, whereas demand for construction and home improvement materials showed signs of recovery.

Stabilizing Prices and Easing Declines.

In 2024, the Producer Price Index (PPI) decreased by 2.2% year-on-year, narrowing its decline by 0.8 percentage points compared to the previous year. From January to July, the PPI decreased from -2.5% in January to -0.8% in July, driven by rising international crude oil and non-ferrous metal prices, a recovering domestic production sector, and a low base effect. However, in August, a dip in global commodity prices led to a 0.7% month-on-month loss, widening its year-on-year decline. Since September, the impact of policy measures and recovering industrial demand has slowed the PPI's monthly decline, with the index turning positive in November and the year-on-year decrease steadily shrinking.

Date: December 20, 2024

In November, the combined effects of macroeconomic policies became more evident. The acceleration of export growth boosted industrial chains, while policies promoting large-scale equipment upgrades and consumer goods trade-ins bolstered manufacturing demand and investment. Infrastructure investment, though slightly decelerating, demonstrated resilience due to the effective execution of existing policies and the accelerated implementation of new measures. Concurrently, strengthened real estate support policies increased transaction volumes; nonetheless, achieving full stabilization requires further recovery in income expectations on the demand side. On the whole, macroeconomic policies are yielding tangible benefits, with key sectors exhibiting promising signs of recovery.

Economic Expansion Gains Further Momentum

In November, the Composite PMI Output Index remained steady at 50.8%, indicating sustained economic growth. The Manufacturing PMI increased to 50.3%, with the Production Index and New Orders Index rising to 52.4% and 50.8%, respectively. Notably, new orders returned to growth for the first time since May, indicating increased demand and market activity. However, the non-manufacturing sector saw mounting pressure as the Business Activity Index dipped to 50.0%. Service output growth moderated slightly to 6.1% year-on-year, down 0.2 percentage points from October.

Exports Remain Stable Amid Fluctuations

From January to November, goods exports increased by 6.7% year-on-year, aligning with the January–October growth rate, indicating strong overall resilience. While November's growth rate decreased by 6 percentage points to 6.7%, it remained among the highest levels this year. Key drivers were front-loading effects and sustained strong demand from the U.S. and ASEAN markets, with U.S. exports surpassing those to Europe. Holiday demand for toys and communication equipment notably enhanced U.S. export growth. However, the EU’s tariffs on electric vehicles tempered gains in the automotive supply chain.

Manufacturing Drives Steady Industrial Growth

From January to November, large-scale industrial output increased 5.8% year-on-year, with November seeing an acceleration of 5.4%. Manufacturing increased by 6.0%, marking its third consecutive month of growth and solidifying its position as the primary driver. Conversely, mining and utilities experienced a slight slowdown from the previous month. Policies promoting new technologies and emerging industries stimulated rapid growth in shipbuilding, smart consumer devices, and lithium battery production. Incentives for new energy vehicles and home appliance upgrades further boosted output. In November, export delivery value increased 7.4% year-on-year, representing the highest monthly growth since August 2022 and providing a strong boost to industrial chains.

Investment Growth Eases Slightly Despite Policy Support

Investment increased 3.3% year-on-year from January to November, with monthly growth decelerating to 2.4% in November. Infrastructure investment slightly decelerated to 4.2%, whereas manufacturing investment maintained a strong pace of 9.3%. Real estate investment declined further to -11.5%, but property sales recorded positive monthly growth for the first time since April 2023, increasing developers' funding sources. Transportation and storage investment declined sharply, whereas gains in power and water infrastructure provided significant support.

Multiple Measures to Bolster and Sustain Consumption Growth

Consumption continued to recover steadily as policies such as trade-ins for new products further stimulated consumer demand, resulting in strong sales across most categories. From January to November, retail sales increased 3.5% year-on-year, maintaining the same pace as the previous period. In November, retail sales grew 3.0%, seeing a slight moderation attributed to early "Double 11" promotions and a strong comparison base from last year. Policies promoting product upgrades led to significant growth in auto and furniture sales, which increased by 6.6% and 10.5%, respectively. Construction and renovation materials saw a resurgence, recording a 2.9% increase. Service-related retail sales also sustained a robust upward trend under the influence of various consumption-boosting measures.

Domestic Prices Gradually Return to Stable Levels

In November, coordinated policies boosted industrial recovery, resulting in a shift in the Producer Price Index from decline to slight monthly growth, reducing its year-on-year shrinkage by 0.4 percentage points. Prices in key sectors, including petroleum extraction, chemicals, and electricity, experienced minor reductions. On the Consumer Price Index (CPI) front, food prices dropped 2.7% month-on-month, markedly above the seasonal average decline over the past decade, mainly attributable to abnormal weather that enhanced agricultural production and logistics. This resulted in a month-on-month decrease of 0.6% in the overall CPI. Non-food prices also fell by 0.1%, indicating weaker demand for travel during the off-season. The decrease in food prices contributed to a moderation in the year-on-year CPI increase, which eased to 1.0%.

Date: Nov 20, 2024

In October, the economy experienced a broad-based recovery from the previous month's lows. This improvement was supported by the latest round of macro policies and a favorable shift in export dynamics. Export growth surged due to timing discrepancies, which, in turn, energized the export-linked industries. The push for equipment upgrades and consumer goods trade-ins buoyed manufacturing demand and investment. Infrastructure investment gained momentum as existing policies took effect and new ones accelerated. Real estate saw a lift in transaction volume due to supportive policies, but a sustained recovery will require improving consumer income expectations. To sum up, policymaking is about trade-offs; fiscal expansion is often more effective than monetary expansion in combating economic downturns. It's imperative to swiftly address the bottlenecks in policy implementation and loosen the reins on individuals to boost the economy.

The economy shows a comprehensive improvement from its recent lows. Key economic activity indicators rose in October compared to September. The manufacturing PMI, non-manufacturing business activity index, and the composite PMI output index increased to 50.1%, 50.2%, and 50.8%, respectively, signaling a broad-based economic upturn. All five major sub-indices for the manufacturing sector increased, and the service sector's business activity index ticked up by 0.2 percentage points to 50.1%, propelling the non-manufacturing business activity index higher. Service production surged 6.3% year-on-year, a yearly peak. A stock market trading boom in October drove the financial sector's production index up by 3.7 points to 10.2%, its highest level this year and a key growth driver. This also contributed to a 5.0% year-on-year increase in the national service sector production index for the January–October period.

Shipping schedule shifts spurred faster export growth. The export growth rate for October surged by 9.6 percentage points to 11.2% compared to September. This momentum propelled the year-to-date export growth rate to 6.7% through the month. Bucking the trend of a typical October lull, this year brought a noteworthy 1.8% increase in exports from the previous month, primarily attributed to typhoon disruptions that postponed some of September's exports to October, resulting in an unexpected year-on-year growth. On a country-specific basis, the export growth rates to major destinations rebounded.

Exports and policies keep industrial growth steady. From January to October, the value-added output of industrial enterprises above designated size rose by 5.8% year-on-year, unchanged from the first nine months. The manufacturing and mining sectors saw a pickup in production, while the utilities sector's growth eased to 5.4%. A resurgence in domestic demand improved the sales-to-production ratio, while the value of exports rose by 3.7% year-on-year. Policies on equipment renewal and consumer goods took effect: car production swung from negative to positive, and the output of new energy vehicles reached a record high. Production of charging piles surged by 25.2%, and industries such as smart consumer devices, shipbuilding, and battery manufacturing have shown substantial value-added growth. The production volumes of agricultural processing, excavating machinery, packaging equipment, and home electric heating appliances have all sustained double-digit growth rates.

Policy efforts keep investment growth on an even keel. From January to October, investment climbed 3.4% year-on-year, matching the pace set during the first nine months. The monthly manufacturing investment growth rate hit 9.9% thanks to large-scale equipment renewals, innovation, and industrial upgrading. Industry-wise, investment accelerated in sectors such as other transportation equipment, non-ferrous metals, food manufacturing, and chemicals. Infrastructure investment also accelerated year-on-year to 4.3%, the first increase since March. The real estate market experienced increased transaction activity, with the year-on-year decline in new commercial housing sales area and sales volume for January to October easing by 1.3 and 1.8 percentage points, respectively, compared to the January–September period. However, such improvement has not yet fed into increased investment.

Policies gave a marginal boost to consumption growth. In October, programs such as consumer goods trade-ins and the "Double 11" shopping spree fueled the year-on-year growth in retail sales, which climbed to 4.8%, up from September. Commodity retail sales growth reached 5%, driven by accelerated sales in home appliances, audio-visual equipment, cultural and office supplies, furniture, and automobiles at retail units above a certain threshold. Necessity consumption remained stable, and discretionary consumption showed modest gains. Auto retail experienced significant recovery, and the real estate chain surged, with the decline in retail sales of building and decoration materials narrowing. As a series of stimulus policies are gradually implemented and service supply is optimized, combined with holiday buzz, service spending is on a fast track.

Active regulation is steering prices towards stability. International crude oil prices dipped due to geopolitical factors, which, in turn, lowered prices in China's oil-related industries. Nevertheless, new policies appear to have revived demand for certain industrial goods, helping to curb the Producer Price Index's (PPI) monthly slide, which shrank by 0.5 percentage points month-on-month. Equipment manufacturing saw price drops due to global economic shifts and domestic sales promotion, slightly widening the PPI's year-on-year decline by 0.1 percentage point. Consumer Price Index (CPI) gains were modest in October, ticking up 0.3% year-on-year, a sign of stable prices overall. Non-food prices declined further by 0.1 percentage points, reflecting market dynamics, while food prices eased back to a 2.9% gain but continued trending upward.

Date: October 20, 2024

During the first three quarters of 2024, a slowdown in overseas demand and increasing uncertainties contributed to a deceleration in year-on-year export growth compared to the first half of the year. Nonetheless, exports continued to drive the development of related industries within the industrial supply chain. The demand and investment in manufacturing were bolstered by policies encouraging large-scale equipment renewals and consumer trade-ins for new products. Additionally, the pace of implementation of infrastructure project reserves increased. Despite existing challenges, China's economic growth rate of 4.8% during the first three quarters still ranks among the top globally. Yet, insufficient demand remains the most significant challenge. This is further exacerbated by the negative growth in public budget revenues and an increased decline in M1 money supply, together signaling a persistent negative economic spiral. To break this cycle and foster a refined economic structure, it is imperative to swiftly implement "macro-micro easing" policies.

Economic factors contributing to an upward economic trend are on the rise. In the first three quarters, the GDP grew by 4.8% year-on-year, a slight deceleration of 0.2 percentage points from the first half of the year. The GDP for the third quarter alone increased by 4.6% year-on-year, marking a 0.1 percentage point decrease from the second quarter. The primary, secondary, and tertiary sectors experienced year-on-year growth rates of 3.2%, 4.6%, and 4.8%, respectively. The manufacturing PMI rebounded to 49.8% in September, with the production index increasing above the critical point for the first time in a month. Concurrent with these trends, the Chinese economy has exhibited several positive developments during the first three quarters. These include the high-tech manufacturing sector consistently outpacing the overall industrial growth rate, a noteworthy pickup in the growth of the service industry, and a steadying growth rate among real estate development investments. These encouraging signs indicate an underlying resilience and dynamism within the economy, suggesting that it remains on a steady course despite broader economic challenges.

A multitude of factors influenced the growth rate of exports. In the first three quarters, exports increased by 6.2% year-on-year, a deceleration of 0.7 percentage points compared with the first half of the year. This trend continued into September, when exports only increased by 1.6% year-on-year, the smallest increase since February 2024. The ongoing decline in the global manufacturing PMI has had a ripple effect, decreasing new export orders to 47.5% in September. Additionally, the above-average number of intense typhoons has further disrupted export shipping activities, exacerbating this situation. Overseas uncertainties, including ongoing trade frictions and the unpredictability of the US election, coupled with negotiations with American dockworkers on the East Coast, have advanced the peak season's arrival. Furthermore, the EU's implementation of anti-subsidy tariffs has led to a cumulative 0.5 percentage point decrease in overall exports compared to the previous month.

Exports supported the stability of related industries. During the first three quarters, the output of industrial enterprises above the designated size increased by 5.8% year-on-year, a rate consistent with the January-August period. It then showed a slight deceleration of 0.2 percentage points from the first half of the year. Additionally, the manufacturing sector saw its growth ease to 6.0%. After four consecutive months of decline, the year-on-year growth rate for industrial enterprises above the designated size rebounded to 5.4% in September. The effect of exports on industrial growth is notable, with the export delivery value of industrial enterprises above the designated size increasing by 4.1% year-on-year during the first three quarters, showing an accelerating trend quarter by quarter. This has spurred significant double-digit year-on-year growth in the export delivery values for export-related manufacturing sectors, such as the automotive, metal products, railway, shipbuilding, aerospace, and aviation industries.

The foundation for an upward trend in investment requires further strengthening. During the first three quarters, the year-on-year growth of total investment was 3.4%, easing by 0.5 percentage points from the first half. Within this change, manufacturing investment saw a year-on-year increase to 9.2%, infrastructure investment slowed to 4.1%, and real estate development investment shrank by 10.1%. In September, investment rebounded with a year-on-year increase of 3.4%, with all three main categories showing higher growth rates than in the previous month, signaling a marginal improvement in investment momentum. Manufacturing investment for September rose by 9.7% year-on-year, with notable acceleration in the textile, general equipment, agricultural and sideline food products, and pharmaceutical manufacturing industries, increasing by 6.3, 7.4, 7.7, and 7.2 percentage points, respectively, compared to the previous month. The other transportation equipment sector saw a substantial year-on-year increase of 37.9%. Infrastructure investment, supported by intensified fiscal measures and faster policy implementation, showed a significant rebound, with all sectors posting higher year-on-year growth rates than in the previous month. The cumulative year-on-year growth of infrastructure investment, including electricity, increased by 1.4 percentage points compared to the previous month, indicating that power sector investment was a key driver in the infrastructure rebound.

Overall consumer spending growth has been weakening amidst fluctuations. Consumer spending growth has been fluctuating and generally weakening. For the first three quarters, the year-on-year increase in total retail sales was 3.3%, a 0.4 percentage point reduction from the first half of the year. In September, the growth rate of total retail sales increased to 3.2%, influenced by the effectiveness of trade-in policies and a low comparative base from the previous year. Commodity retail sales saw a year-on-year increase of 3.3%, with sales by larger retailers increasing by 2.8%, indicating a return to positive growth. Essential and discretionary consumer spending remained robust, while the real estate-related consumption chain saw a notable recovery. Localized efforts to enhance trade-in policies have boosted sales of automobiles, home appliances, and related products. However, service consumption showed signs of weakening. From January to September, the cumulative year-on-year growth rate of service retail sales slowed to 6.7% compared to the January–August period, and the year-on-year growth rate of catering income fell to 3.1% in September.

The Producer Price Index (PPI) is anticipated to decrease further in its year-on-year decline. For the first three quarters, the PPI decreased by 2.0% year-on-year, which is a slight improvement of 0.1 percentage points from the first half. In September alone, the PPI decreased by 2.8% year-on-year, a worsening of 1.0 percentage point from August. International factors have led to a slowdown in price increases for industries associated with oil and non-ferrous metals. The real estate market continues to adjust, and prices in related industries such as steel and cement have been weak. Meanwhile, the Consumer Price Index (CPI) for the first three quarters increased by 0.3% year-on-year, expanding by 0.2 percentage points from the first half. This was mainly due to increases in non-food prices. With additional policies pending and the gradual implementation of existing measures, the PPI's upward momentum is expected to regain strength. This could lead to further narrowing of the PPI's year-on-year decline, not only in October but also throughout the fourth quarter.

Date: August 20, 2024

Export growth recovered in August, and policy support bolstered manufacturing investment. However, growth in infrastructure investment and physical work volume were supressed. As real estate policies have been implemented, more measures are expected to boost market confidence. Consumer spending growth has slowed, with industrial and consumer goods prices remaining low. Public budget revenues and monthly consumption in top-tier cities fell, the decline in M1 money supply widened, and urban surveyed unemployment rates rose beyond seasonal patterns—all pointing to economic weakening compared to July. It is critical to resolve the issues at the next stage underlying the economic and non-economic mechanisms causing this slowdown, to balance growth speed and quality, and to emphasize the impact of the economic performance on public well-being and external cooperation.

Be vigilant against the economic downward spiral. In August, the composite PMI output index dropped by 0.1 percentage points to 50.1%, its lowest since January 2023, with the manufacturing PMI down 0.3 points, being the main drag. Key sub-indices, such as production and new orders, remained below critical levels and worsened than the previous months, indicating a worsening contraction cycle in manufacturing, characterized by "weakened new orders–reduced production–shrinking raw material inventories–weakening employment–and delayed deliveries." While the non-manufacturing business activity index saw a slight rise, driven by the services sector, other indicators remained generally sluggish.

Specific industries contributed to a rebound in export growth. Exports increased by 1.7 percentage points month-on-month in August, reaching 8.7%, the highest since March 2023. This was partly due to delayed shipments caused by typhoon disruptions in late July, which moved some goods initially scheduled for export in July into August. Additionally, the peak season for consumer electronics restocking and the launch of new products resulted in a rise in exports, further boosted by demand spurred by the application of AI. Consequently, smartphone exports climbed to 16.9%, contributing 0.6 percentage points to overall export growth.

Exports supported the stability of related industries. Although the year-on-year growth rate of industrial enterprises above the designated size dipped to 4.5% in August owing to a higher base of the same period last year, the two-year average growth accelerated to 4.5%. Among the three major categories, the manufacturing and mining industries saw decelerated growth, whereas the growth rate of electricity, thermal power, gas, and water production and supply industries accelerated to 6.8%. The mining sector’s slowdown indicates a deceleration in upstream inventory replenishment. Export-linked industries continued to perform well, with export deliveries in sectors such as automotive and general equipment maintaining double-digit growth.

Multiple factors continued to impede investment growth. From January to August, investment growth slowed by 0.2 percentage points to 3.4% compared to January–July, with total private investment plummeting to -0.2%. Breaking it down into three major categories: infrastructure investment growth slowed by 0.5 percentage points, manufacturing investment growth slowed by 0.2 percentage points, and real estate development investment maintained the same decline. Infrastructure was the main drag on the deceleration of investment growth, possibly due to extreme heat and rainfall disrupting construction activities as well as the slow implementation of funded projects. However, from January to August, investment in high-tech manufacturing was 0.5 percentage points higher than the overall manufacturing sector, driven by large-scale equipment renewals, which saw equipment purchase investments surge by 16.8%.

Consumption weakens as low base effects fade. In August, total retail sales of consumer goods increased by 2.1% year-on-year, down 0.6 points from the previous month. Commodity retail sales fell 1.9%, whereas summer travel helped boost catering revenues by 3.3%. However, slower residents' income growth resulted in weaker retail sales growth in both urban and rural areas.

More measures are required to stabilize prices. In August, affected by insufficient market demand and the downward trend in prices of several bulk commodities, production material prices in energy-intensive industries weakened, resulting in a month-on-month and year-on-year decline in the Producer Price Index (PPI). The expanding drop in PPI structurally dragged down the Consumer Price Index (CPI). However, disturbances such as high temperatures and rainy weather pushed the CPI up by 0.6% year-on-year, with food prices driving the increase. Among them, the rise in prices of fresh vegetables and fruits was the primary driver.

Date: August 20, 2024

In July, export growth slowed compared to the previous month amid global manufacturing volatility and increasing international uncertainties. Local infrastructure development remained sluggish, and the real estate sector continued to struggle. Although consumer spending saw a modest increase, its sustainability remains uncertain. Industrial product prices continued to fall and consumer prices stayed low. These challenges were further underscored by negative growth in public budget revenue, lower monthly consumption in first-tier cities, and a decrease in M1 money supply, signaling a broader downturn in economic prosperity. In response, it is essential to address the systemic adverse effects of sustained low prices, closely monitor shifts in micro-incentives, and swiftly enhance primary entity incentives to stimulate sustained economic recovery.

The foundation for economic recovery requires further strengthening.

Over the same period, the manufacturing PMI dipped to 49.4%, signaling ongoing contraction, while the non-manufacturing activity and composite PMI output indexes slipped to 50.2%, reflecting growth deceleration. In the manufacturing sector, the production index fell to 50.1%. The service industry also saw a decline, with the business activity index falling to 50.0%. However, in sectors closely related to travel and consumption, such as railway and air transport, the business activity index remained robust, staying above 55.0%. In contrast, the construction industry's business activity index declined to 51.2%.

External demand turbulence slowed export growth.

Global manufacturing shifts and rising international uncertainties dampened export growth in July compared to the previous month. Regionally, while exports to Europe and the US increased, shipments to ASEAN, South Korea, Japan, and other Asian economies declined. By category, technology-intensive goods outperformed labor-intensive goods. On one hand, a resurgence in global demand for consumer electronics boosted exports along the computer and electronics supply chain. On the other hand, waning demand related to international events like the Paris Olympics reduced labor-intensive product exports.

Exports supported the overall stability of the industrial sector.

In July, the added value of the industrial enterprises above designated size eased by 0.1 percentage points to 5.9% compared to the previous month. Overall, exports remained the primary growth driver, with the cumulative growth rate of export delivery values for these enterprises increasing monthly since the beginning of the year. In July, export delivery values grew by 6.4% year-on-year, surpassing June’s growth rate. The electronics sector, a major export industry, experienced accelerated year-on-year growth in export delivery value, providing significant support. The automotive industry also maintained double-digit export delivery value growth for eight consecutive months. Additionally, the general and specialized equipment and chemical industries reported double-digit growth in export delivery values, possibly due to front-loading exports.

Multiple factors slowed investment growth.

From January to July, investment grew by 3.6%, a decrease of 0.3 percentage points compared to the first half of the year. A closer look at the sectors reveals that investment in manufacturing, infrastructure, and real estate slowed relative to the first half of the year. Infrastructure investment growth fell to 4.9% year-on-year due to the slow issuance of new special bonds and challenges in local government financing. Despite supportive policies, few cities experienced a market rebound, with housing prices remaining sluggish and homebuyers adopting a strong wait-and-see attitude.

A low base led to a rebound in consumer spending growth.

Retail sales growth rebounded due to a lower base compared to the same period last year, as well as a boost from summer travel and consumption-boosting policies. In July, the year-on-year increase rose by 0.7 percentage points to 2.7% compared to June. However, declines in overall income and wealth led to a heightened saving preference among residents, keeping consumer spending growth for enterprises above the designated size sluggish, with a growth rate of only -0.1%. Amid the summer travel season, the potential for service consumption continued to be unleashed. From January to July, service retail sales grew by 7.2% year-on-year, outpacing the growth of goods retail sales during the same period.

The persistent decline in prices needs to be reversed promptly.

From January to July, the year-on-year decline in the Producer Price Index (PPI) narrowed by 0.1 percentage points from the first half of the year, reaching -2.0%. Insufficient market demand and falling prices for some international bulk commodities contributed to a continued decline in the July PPI, with both month-on-month and year-on-year growth figures falling at the same rate as the previous month. The main drivers of the PPI drop were falling prices in the ferrous metals, non-metals, and equipment manufacturing industries. On the Consumer Price Index (CPI) front, high temperatures and rainfall drove up the prices of fresh vegetables and eggs, while strong summer travel demand increased the cost of flights and accommodation. As a result, the CPI increased by 0.5% year-on-year in July, with pork prices surging by 20.4%, significantly contributing to the rise.

Date: Jul 20, 2024

In the first half of 2024, export growth accelerated due to global manufacturing recovery, and consumer goods sales remained steady thanks to supportive policies and other factors. However, the sustained decline in industrial product prices and the persistently low consumer prices suggest that demand remains relatively weak. The real estate market remains sluggish, overall societal expectations are still low, and businesses are under significant operational pressure. To turn the tide, it's crucial for policies to be significantly ramped up as soon as possible to improve expectations and boost confidence in the economy.

The economy showed signs of expansion, but faced mounting pressures.

In the first half of the year, the GDP increased by 5.0% year-on-year at constant prices, marking a slowdown from the same period last year and the entire previous year. The growth rate was 5.3% in the first quarter, but decelerated to 4.7% in the second quarter. The primary sector saw a year-on-year growth of 3.6% in the current quarter, while both the secondary and tertiary sectors experienced a noticeable decline. The swift slowdown in the growth rate of the tertiary sector's GDP could be attributed to adjustments in the statistical approach of the financial industry, reflecting the overall economic strain.

Recovery in external demand drives export acceleration.

In the first half of the year, exports grew by 6.9%, significantly outpacing the same period last year and the entire previous year. According to the latest statistics released by the WTO, the global manufacturing prosperity index continued to rise in the second quarter, and the trade-weighted manufacturing PMI rebounded. Influenced by the global trade recovery, exports in June registered a year-on-year increase of 8.6%, up 1 percentage point from the previous month, reaching the highest point since January 2024. The trade surplus in goods reached its highest since historical data began in August 1994. Despite a significant improvement in the volume of exports since the beginning of the year, the prices of exports have remained low.

Exports contributed to the overall stability of the industrial sector.

In the first half of the year, the added value of the industrial enterprises above designated size grew by 6.0% year-on-year, with the first and second quarters seeing respective increases of 6.1% and 5.9%. Among the three major sectors, manufacturing saw a robust growth of 6.5%, while the electricity, heat, gas, and water production and supply sector grew by 6.0%. The mining industry, however, experienced a more modest increase of 2.4%. Collectively, this indicates a slight overall deceleration in the growth rate. The high-tech manufacturing sector has been a standout, leading the way in high-end manufacturing. The added value of high-tech manufacturing industries above designated size surged by 8.7% year-on-year in the first half of the year, up by 1.2 percentage points compared to the first quarter. Driven by the rebound in exports, the cumulative growth rate of export delivery value for industrial enterprises above designated size has been accelerating month by month. This upward trajectory has been sustained for five consecutive quarters since the second quarter of 2023, underscoring the sector's resilience and growth momentum.

A variety of factors led to a continued decline in overall investment.

In the first half of the year, investment grew by 3.9% year-on-year, marking a slowdown from the first quarter but an acceleration compared to the same period last year and the entire previous year. From the perspective of three areas: Infrastructure investment rose by 5.4%, manufacturing investment by 9.5%, while real estate investment fell by 10.1%, with all these sectors seeing a decrease from the first quarter. Since the beginning of the year, regions have been proactive in initiating projects funded by additional government bonds and accelerating post-disaster reconstruction efforts. However, a slow fiscal tempo and the strain on fiscal spending have led to a continuous decline in narrowly defined overall infrastructure investment. The new real estate policies have started to take effect, with the year-on-year decrease in real estate investment narrowing for the first time this year.

The deceleration in the growth of consumer spending requires close attention.

In the first half of the year, China's total retail sales of consumer goods increased by 3.7% year-on-year, a slowdown compared to the first quarter, the same period last year, and the entire previous year. Among these, retail sales of goods rose by 3.2%, catering services saw a growth of 7.9%, and the retail sales of services were up by 7.5% year-on-year. Overall, the performance has weakened compared to the first quarter.

The persistent decline in prices needs to be reversed promptly.

In the first half of the year, the Producer Price Index (PPI) fell by 2.1% year-on-year, marking a 0.6 percentage point decrease in the rate of decline compared to the first quarter. The overall upward trend in international prices for crude oil and non-ferrous metals has led to increased prices in related domestic industries. Prices in sectors such as coal, building materials, and equipment manufacturing have seen a reduction in the rate of decline. Policies including large-scale equipment renewal and trade-ins of old consumer goods for new ones are gradually being implemented and are beginning to take effect, contributing an improved outlook for the steel market. The slowing decrease in PPI is contributing to a recovery in the Consumer Price Index (CPI), but the ongoing negative growth in PPI continues to exert downward pressure on the CPI. There has been a slight decline in the growth rate for service prices: in the first half of the year, service prices were up by 0.9% year-on-year, with the growth rate falling by 0.2 percentage points from the first quarter.

Date: Apr 20, 2024

In the first quarter of 2024, the economy improved overall due to the combined effect of recovering external demand, the sustained impact of earlier policies, the timing of the Spring Festival, and changes in base figures. Major macroeconomic indicators remained generally stable, but data for March showed signs of marginal weakening compared to January and February. This weakening is partly due to the base effect but also requires close attention, indicating the need for sustained policy efforts.

Policies, among other factors, have contributed to the overall economic improvement. In the first quarter, GDP grew by 5.3% year-on-year at constant prices, accelerating compared to both the fourth quarter and the entire previous year. The secondary industry played a significant role in this growth, with industrial added value increasing by 6.0% year-on-year, and manufacturing added value rising by 6.4%. Moreover, modern service industries maintained a strong development momentum: in the first quarter, the added value of information transmission, software and information technology services, leasing and business services, and financial services grew by 13.7%, 10.8%, and 5.2% year-on-year, respectively, collectively driving a 2.7 percentage point increase in the service industry’s added value. Marginally, the composite PMI output index, the manufacturing PMI, and the non-manufacturing business activity index all rose in March compared to the previous month, and all remained above the threshold line, indicating accelerated economic expansion.

A low base and external demand have bolstered improvements in exports. In the first quarter, exports and imports, denominated in RMB, grew by 4.9% and 5.0% respectively year-on-year, marking a rebound from the previous year’s fourth quarter. Looking regionally, while growth in exports to developed economies like the United States and the European Union slowed, there was a resurgence in growth in exports to Japan, South Korea, and the Chinese Taiwan region, with a concurrent recovery in growth in exports to ASEAN countries. In terms of products, driven by the rebound in global demand and the concurrent upturn in the global semiconductor cycle, exports of computer electronics industry chain products, represented by integrated circuits and automatic data processing equipment, saw a seasonally adjusted increase. Notably, March saw increased export growth rates for mobile phones, integrated circuits, and automatic data processing equipment, sequentially boosting the overall export growth rate by 0.5, 0.3, and 0.2 percentage points respectively compared to the previous month.

The growth rate of industries above designated scale accelerated overall. In the first quarter, industries above designated scale grew by 6.1% year-on-year, marking a 0.1 percentage point increase in growth compared to the fourth quarter of the previous year, continuing the trend of recovery. Looking at the three major categories, the growth rate of manufacturing increased by 0.4 percentage points to 6.7% compared to the fourth quarter of the previous year, while the growth rate of electricity, heat, gas, and water production and supply increased by 0.5 percentage points to 6.9%, both being the main drivers behind industrial recovery. Influenced by factors such as the timing of the Spring Festival and slow resumption of infrastructure and construction activities, the capacity utilization rates of industry and manufacturing fell to 73.6% and 73.8%, respectively, in the first quarter.

Policies, among other factors, have contributed to the rebound in investment growth. In the first quarter, the year-on-year growth rate of investment accelerated by 0.3 percentage points to 4.5%, compared to January and February, and increased by 1.5 percentage points compared to the previous year. Investment growth excluding real estate, however, reached 9.3%, highlighting the continued significant impact of real estate on investment growth. With the impact of policy support and other factors, investment growth in the high-tech manufacturing sector accelerated by 0.8 percentage points to 10.8% year-on-year in the first quarter, compared to January and February, and in turn drove investment growth in manufacturing to 9.9%.

Overall, consumer spending growth remained relatively stable in the first quarter. Total retail sales of consumer goods grew by 4.7% year-on-year, indicating slight slowing trends. As consumption policy measures were implemented, consumer potential accelerated, and commodity consumption steadily rebounded. Sales of essential goods were robust, with retail sales of grain and oil products and beverages increasing by 9.6% and 6.5% respectively. From a marginal perspective, the year-on-year growth rate of total retail sales of consumer goods slowed significantly to 3.1% in March, possibly due to a higher base last year. Meanwhile, rapid growth in consumption of travel and entertainment-related services continued to drive consumer spending.

Date: November 20, 2023

In October, China's economy may not appear to gain a strong recovery. However, a rational look at the situation shows there is some potential amid the current difficulties. Weakness in overseas manufacturing led to a decline in exports, impacting relevant industrial chains. Infrastructure and real estate investments remained weak, while manufacturing investment stayed stable owing to policy support and shifting demands. Supported by holiday promotions and a resurgence in service consumption, overall consumption remained resilient, although certain consumer goods experienced a slowdown in growth. Continuous decline in indicators including the Consumer Price Index (CPI) revealed the need for further stimulus including policy support to bolster internal momentum for economic growth.

October witnessed a slight decline in the Purchasing Managers’ Index (PMI), indicating a slowdown in the pace of overall economic expansion. The Composite PMI Output Index, Manufacturing PMI, and Non-Manufacturing Business Activity Index stood at 50.7%, 49.5%, and 50.6% respectively, dropping by 1.3, 0.7, and 1.1 percentage points compared to the previous month. All five sub-indices within the Manufacturing PMI registered decreases, signaling a deceleration in manufacturing production expansion, intensified demand contraction, reduced main raw material inventories, reduced labor use, and quicker delivery times from raw material suppliers. Furthermore, the Index of Service Production and Industrial Added Value demonstrated a slight acceleration compared to the previous month, primarily due to the base effect. While there was an increase in the year-on-year growth rate for October, the overall trend reveals a decline in the two-year compound annual growth rate for 2021-2023.

In October, exports were mainly influenced by seasonal factors and the global downturn in manufacturing industry prosperity. Regarding seasonality, there was an 8.1% month-on-month decrease in October’s exports, signaling ongoing instability in global demand. The global Manufacturing PMI dropped to 48.8%, reaching its lowest since July 2023. The growth in China’s exports to several regions also declined. In terms of products, the end of Christmas shipments led to a decline in the export growth rate of labor-intensive products. Simultaneously, the European Union’s anti-subsidy investigation into China’s new energy vehicles hindered the export growth of the automotive industry chain. Moreover, the export growth in the electronic industry chain displayed a divergence, with an uptick in mobile phone exports but a more significant decline in the exports of automated data processing equipment and integrated circuits.

For industrial enterprises above designated size, the year-on-year growth rate in October reached 4.6%, slightly up from the previous month, while the industrial growth rate from January to October slightly increased to 4.1%. Mining and manufacturing emerged as the primary drivers of growth, especially noticeable in the continuous three-month upturn in equipment manufacturing. However, after excluding the base effect, regarding the two-year compound annual growth rate, October saw a year-on-year growth rate of 4.8% for industrial enterprises above designated size, slightly down from the previous month. This decline was mainly due to specific industries stocking up ahead of time, resulting in the release of a portion of production demand last month. Inadequate foreign demand affected export-related manufacturing, while diminishing domestic demand in infrastructure and real estate investment continued to weaken related industrial chains.

October registered an overall year-on-year investment growth rate of 2.9%, showing a slight decrease compared to the previous month. Manufacturing investment remained stable, but there was a continued decline in both infrastructure and real estate investments. The slowdown in infrastructure investment growth can be attributed to factors such as a high base effect and a slowdown in the issuance of special bonds. Except for electricity, heating, and hydraulic power, the year-on-year growth rate in other sub-items has declined. Manufacturing investment experienced a slight dip, along with reduced investment in high-tech industries, automobile manufacturing, electrical machinery and equipment manufacturing, computer communications, and other electronic equipment manufacturing. Real estate investments, sales volume, sales area, and funding sources continued to weaken. Private real estate investment showed a marginal rebound overall, particularly noticeable when excluding real estate development investment, signaling a gradual recovery in the confidence for investment among private enterprises.

From January to October, there was a 6.9% year-on-year increase in retail sales of consumer goods. Notably, automobile consumption helped to boost overall consumer spending in October. From January to October, service retail sales saw a slight improvement with a 19.0% year-on-year growth. The effect of new energy vehicle policies started to be felt and resulted in an 11.4% growth in retail sales of passenger cars. The adjustment of policies in the real estate market also led sectors like home appliances, furniture, and building decoration to turn positive after 12 months. Regarding service consumption, the year-on-year growth rate of catering services rose to 17.1%. However, it is worth noting that the rebound in the growth rate of total retail sales of consumer goods was significantly influenced by a low base effect.

Date: Feb 27, 2023

Because of Chinese New Year, the statistics bureau didn’t announce price, financial and PMI data until February. China switched from zero-COVID lockdown to almost no restrictions in December 2022, and by January 2023, normal life had nearly returned. The economy is generally improving, but caution about its sustainability is required.

Manufacturing PMI, the non-manufacturing business index and the composite PMI production index were 50.1%, 54.4%, and 52.9% in January 2023, up 3.1, 12.8, and 10.3 pps from December. All rose to the improvement zone, showing that the economy is recovering. Our in-depth analysis instead shows that the improvement is still mainly from infrastructure investment. Our survey data shows most industries and firms are only the same or in slightly better shape than in January 2022 - not a big jump from the zero-COVID policy period.

In January 2023, PPI fell -0.4% m/m, growing -0.8%, down 0.1 pps, largely because of falling oil and coal prices. CPI mildly increased. CPI rose 2.1% y/y in January, up 0.3 pps from December 2022. The rise is from demand release after pandemic control relaxation and the New Year’s holiday effect.

Monetary policy expanded. At the end of January, M1 rose 6.7% y/y, up 3 and 8.6 pps from December 2022 and January 2022, respectively. M2 rose 12.6% y/y, up 0.8 and 2.8 pps from the end of December and January 2022, reaching its peak since April 2016. The increase is due to both household deposits and enterprise loans, showing monetary policy expansion.

Chinese banks extended record lending in January, after authorities prodded them to lend more to businesses, though consumer borrowing remained subdued. In particular, financial institutions offered 4.9 trillion yuan of new loans, above the 4.2 trillion yuan estimated by economists on average, and from the earlier record of 3.98 trillion yuan a year ago. Part of the loan increase was moved from bond financing. Although this news is positive, we don’t expect economic recovery to be as strong as other analysts forecast, since consumer confidence is low.

Date: Jan 29, 2023

GDP grew 3% in 2022. Specifically, China’s economy rose by 2.9% y/y in Q4 2022, down from the 3.9% growth reported in Q3. Many negative factors affected the economy in 2022, including global macroeconomic tightening, the Ukraine crisis, real estate restructuring, the pandemic management policies and so forth. As some of the above factors abated, particularly abolishment of the zero-COVID policy, we expect that, after a turbulent 2022, the economy will be back on track in 2023.

Industrial output grew 3.6% in 2022, down 6 pps from 2021. Investment rose 5.1%, up 0.2 pps, driven mainly by state investment. Consumption fell significantly, by -0.2% y/y, from 2021, down 12.7 pps, from repeated lockdowns.

Exports rose 10.5%, down 10.5 pps from 2021. Exports’ monthly growth rates displayed a downward trend. Net exports’ contribution to GDP only accounted for 0.5 pps. Particularly in Q4, the share of exports in accounting for GDP growth is only -1.2 pps, negatively impacted by weak global demand and the dramatic change in domestic COVID policy.

Prices are instead facing deflation risk. In 2022, PPI rose 4.1% and CPI rose 2%. However, both displayed slowing trends. In December, PPI and CPI only grew -1.1% and 1.8% y/y. Monetary policy is still stable. M1 rose 3.7% y/y, down 0.9 pps. M2 increased 11.8% y/y, down 0.6 pps, partially reflecting weak money demand.

A series of government policies is being released to stabilize the real estate market, while discouraging speculation. On January 5th, the People’s Bank of China announced that it would allow banks in cities that experienced housing price declines to cut mortgage rates for first-time house buyers. This directive followed last month’s meeting by top national leaders, which typically gives guidance in line with the coming year’s main economic theme, and this year stated that housing consumption would be a significant way to expand national consumption. We believe the housing market will mildly strengthen this year, but not thrive. Positive factors are the abandoning of any pandemic restriction, the banking sector’s efforts to keep most real estate developers solvent and the already relatively low base number.

Date: Nov 24, 2022

Growth is weakly recovering, with pressure ahead largely from the Covid prevention and its related lockdowns. Although there was some rumor regarding abandoning the zero-Covid policy, there were also signs that China will commit to this policy in the short term, citing reasons from state media that China’s per capita medical resource is low. We forecast that although there might be some relaxing adjustment, for example that foreign entry has reduced to five-day quarantine from seven days, the zero-Covid policy will not be abandoned soon.

In January-October, industrial output rose 4% y/y, continuing its weak recovery since May. Investment rose 5.8% y/y, down 0.1 pps from first three quarters. China’s PMI, manufactural PMI, and non-manufactural business activity index were 49%, 49.2%, and 48.7%, down 1.9, 0.9, and 1.9 pps from September.

Retail sales of social consumption goods fell -0.5% y/y, down 3 pps from September. Exports in October rose 7% y/y, down 3.7 pps from September. The global weakening demand is the main reason behind slower exports and very likely to persist in the medium term.

Economic slowdown is driving down prices. PPI fell -1.3% y/y, down 2.2 pps from September. CPI rose 2.1% y/y, down 0.7 pps from September. The global interest rate increase to combat inflation has limited Chinese central bank’s ability to cut interest rate to support the economy. Loan demand is weak. M1 rose 5.8% y/y, down 0.6 pps. M2 rose 11.8% y/y, down 0.3 pps.

On November 11th, Beijing unveiled a 16-point plan that significantly eases a crackdown on lending to the real estate sector, leading to property developers’ share instantly increase by 11%. Key measures include allowing banks to extend maturing loans to developers, supporting property sales by reducing previous sale restrictions, boosting other funding channels, and ensuring the delivery of pre-sold homes to buyers. We believe these policies will calm the market and make real estate cooling milder, but unlikely to reverse the downward trend immediately. However, real estate collapse or systemic risk can be avoided.

Growth strengthened, but only slightly. In August, industrial output rose 4.2% y/y, up 0.4 pps, lifting overall January-August growth to 3.6%, up 0.1 pps. Investment rose 5.8% y/y in January-August, up 0.1 pps. The August growth rate was 6.4% y/y, up 2.8 pps. Real estate investment growth rate fell further, to -13.8% y/y, down 1.7 pps from August 2021.

In August 2022, consumption rose 5.5% y/y, up 2.7 pps. This is partly due to the low base number of last year, when consumption rose 2.5%, and was down 6 pps from August 2021.

Exports rose 11.8% y/y, down 12.1 pps from July 2022. This seems partially because all major countries except China are exiting from monetary expansion, leading to weakened demand. This month was the first time where exports to the United States had negative growth of -3.8% y/y, dragging down total export growth by 3 pps.

PPI rose 2.3% y/y in August, down 1.9 pps. A major contributing factor is that the production material price growth rate was down 2.6 pps. CPI rose 2.5% y/y, down 0.2 pps from July. Monetary policy remained neutral. At the end of August, M0 rose 14.3% y/y, up 0.4 pps from July. M1 increased 6.1% y/y, down 0.6 pps from July. M2 rose 12.2% y/y, up 0.2 pps.

The offshore exchange rate of the Chinese yuan versus the U.S. dollar recently breached the 7:1 mark for the first time in over two years. Similar to other global currencies that have depreciated in 2022, the yuan’s decline is being driven by the strengthening of the dollar. However, the yuan “basket index” has been relatively stable, and the yuan is unlikely to see significant depreciation, given our forecast of a good balance of payments and overall macroeconomic recovery from further stimulative fiscal policy in the coming months. Other major currency determinants are also sound for the yuan, including a high position for the interest rate and foreign reserves.

Industrial output grew 3.5% y/y in January-July, up 0.1 pps from H1. In January-July, investment rose 5.7% y/y, down 0.4 pps from H1. In particular, the investment growth rate in July was down 2.4 pps from June. High infrastructure investment has been flattened by reduced real estate investment.

Retail sales of social consumption goods fell -0.2% y/y in January-July, up 0.5 pps from January-June. Exports were still strong. In July, exports rose 23.9% y/y, up 1.9 pps from June. Due to the stop of global monetary policy easing, the continuing Ukraine crisis, and the ongoing pandemic, other countries have not recovered well, giving more opportunities to Chinese companies.

PPI and CPI continued to converge. In July, the global crude oil price dropped significantly, leading the overall price level in China to fall. PPI rose 4.2% y/y, down 1.9 pps. CPI rose 2.7% y/y, up 0.2 pps from June, mainly driven by food prices. Monetary policy is easing, but at a small scale due to inflation concern. In the end of July, M0 rose 13.9% y/y, up 0.1 pps from June. M1 rose 6.7% y/y, up 0.9 pps. M2 rose 12% y/y, up 0.6 pps.

The real estate market has been cooling for over a year, and has become particularly cold. In August, China’s property sales plunged almost a third, more than during the 2008 financial crisis. Real estate investment growth fell further to -12.3%, after falling -9.4% in June and -10.1% in April. The real estate sector takes one third of GDP, and so receives much attention. We view the picture as completely different from the 2008 U.S. housing crisis. It is the Chinese government who started this real estate deleveraging, in view of potential future financial problems, and so it is largely manageable. There are also complementary policies, such as bailing out home buyers. Risk is containable, but the process is painful, and will take some time.

GDP only grew 2.5% y/y in H1. As the pandemic shock has been gradually under control and the start of various economic stabilization policies, the recovery growth in June has lifted the Q2 growth to achieve positive growth at 0.4% y/y, contributing to the path “back to normal”.

In H1, industrial output rose 3.4% y/y, down 3.1 pps from Q1. In H1, investment growth rate was 6.1% y/y, down 3.2 pps from Q1, but still 1.2 pps faster than 2021. The continuing real estate cooling does not see any time ending.

Pandemic lockdowns suppressed consumption. Retail sales of social consumption goods fell -0.7% y/y, down 4 pps from Q1. Survey data shows Chinese consumers are pessimistic about future income growth putting more constraint on future consumption recovery. In H1, exports rose 13.2% y/y. In June alone, exports rose 22% y/y, accelerating since April, and is an important force lifting economic recovery.

In H1, PPI rose 7.7% y/y. CPI increased 1.7% y/y. Low inflation benefits from the recovery of supply chains, domestically and internationally. However, future inflation pressure is still high. The main financial indicators were loosened somewhat countercyclically. At the end of June, M2 rose 11.4% y/y, up 0.3 pps from May, and up 1.7 pps from Q1, slowly picking up. M1 rose 5.8% y/y, up 1.2 pps from May, and up 1.1 pps from Q1.

China’s unemployment situation is worsening. According to the National Bureau of Statistics, the government official source, China’s youth unemployment rate for ages from 18 to 24 hit an all-time high of 19.3% in June. It was a sharp rise from 18.4% in May and marked a year-on-year increase of 25%. We believe the unemployment might not pose a society crisis. Parents in China usually provide living net. The unemployment leans more to friction cause. For example, many campus recruitments were suspended because of the pandemic.

Government will continue its effort to bring the economic activities to a higher level. However, it seems not necessary for China to stimulate the economy by additional measures. On July 20th, China’s Prime Minister Li Keqiang stated that China will not adopt large stimulus policies.

Because of the long Chinese New Year holiday, the statistics bureau only announced price, financial and PMI data in February. Producer prices grew more slowly. PPI rose 9.1% y/y, down another 1.2 pps from December. The ex-factory price index of industrial goods rose 8.85% y/y, while CPI growth also slowed. CPI rose 0.9% y/y in January, down 0.6 pps from December. In particular, food prices fell -3.8% y/y, down 2.6 pps from December, dragging CPI down 0.72 pps. That is the leading factor lowering CPI. The falling price levels offer ample room for further money expansion.

At the end of January, M2 rose 9.8% y/y, up 0.8 pps from the end of December, and up 0.4 pps from January 2020. M2 is not strongly affected by the Spring Festival effect. The significant trending upward reflects expansionary monetary policy. M1 fell -1.9% y/y. The adjusted growth rate after taking out the effect of the New Year’s holiday was around 2%. M0 rose 18.5% y/y, a major increase.