Innovative, Objective, Practical

And it's not just about shipping more units. Chinese manufacturers are now designing products that fit the way Europeans actually live, from portable units that bypass strict installation rules to gadgets that offer sun protection too. Zhao Chenchen takes a closer look.

Umbrellas, mini fans, and ice makers. The demand for these cooling appliances from China surges as Europe experiences another summer of extreme heat. And Chinese manufacturers are redesigning these products to better fit local lifestyles.

ZHAO CHENCHEN Foshan, Guangdong Province "This is a mobile split air conditioner tailored for the European market. The top module, which only weighs about 10 kilograms, functions as the outdoor condenser, and it can be easily mounted onto a windowsill without requiring structural drilling."

XIONG XUEQIN Sales Director, Midea RAC Europe Region "In Europe, the rental rate is relatively high, and people want products that can be used right away. Compared to traditional mobile air conditioners, it has higher energy efficiency to save your electricity bill and better noise control as its external unit is outdoors. That's why it can win the hearts of European consumers."

A product like this was born out of a localized approach. European consumers did not have the demand to purchase air conditioners until recent years. But with a global designing team, Chinese enterprises can respond faster with local insight.

ZHAO ALI Europe Product Manager, Midea RAC Overseas "We started from the product, with the front-end team identify a specific problem from the local consumers. Then we bring together a dedicated team to develop a solution, working closely with our R&D teams in China as well as our industrial design team in Italy."

Sales of this AC in Europe have more than doubled to some 200,000 units this year. More Chinese manufacturers are designing products around local consumer needs, from portable fans for outdoor lifestyles in Latin America to energy-efficient climate solutions for European homes. Expert says innovation no longer stops at the factory floor.

LIU ZHIJIE Director, International Cooperation Department China Development Institute "It's about tech innovation. We've long moved from the model of original equipment manufacturing. Chinese companies can now turn independent R&D into products fast , driven by the market demand."

With an expanding China–Europe freight train network, some shipments can now reach Europe in as little as 15 days. That's around 25 days faster than traditional sea freight. As summer demand gradually gives way to the heating season, production lines are already preparing for the next wave of orders.

Designing smarter, responding faster, and staying closer to the markets they serve are becoming the key competitiveness for Chinese manufacturers. (Zhao Chenchen, CGTN)

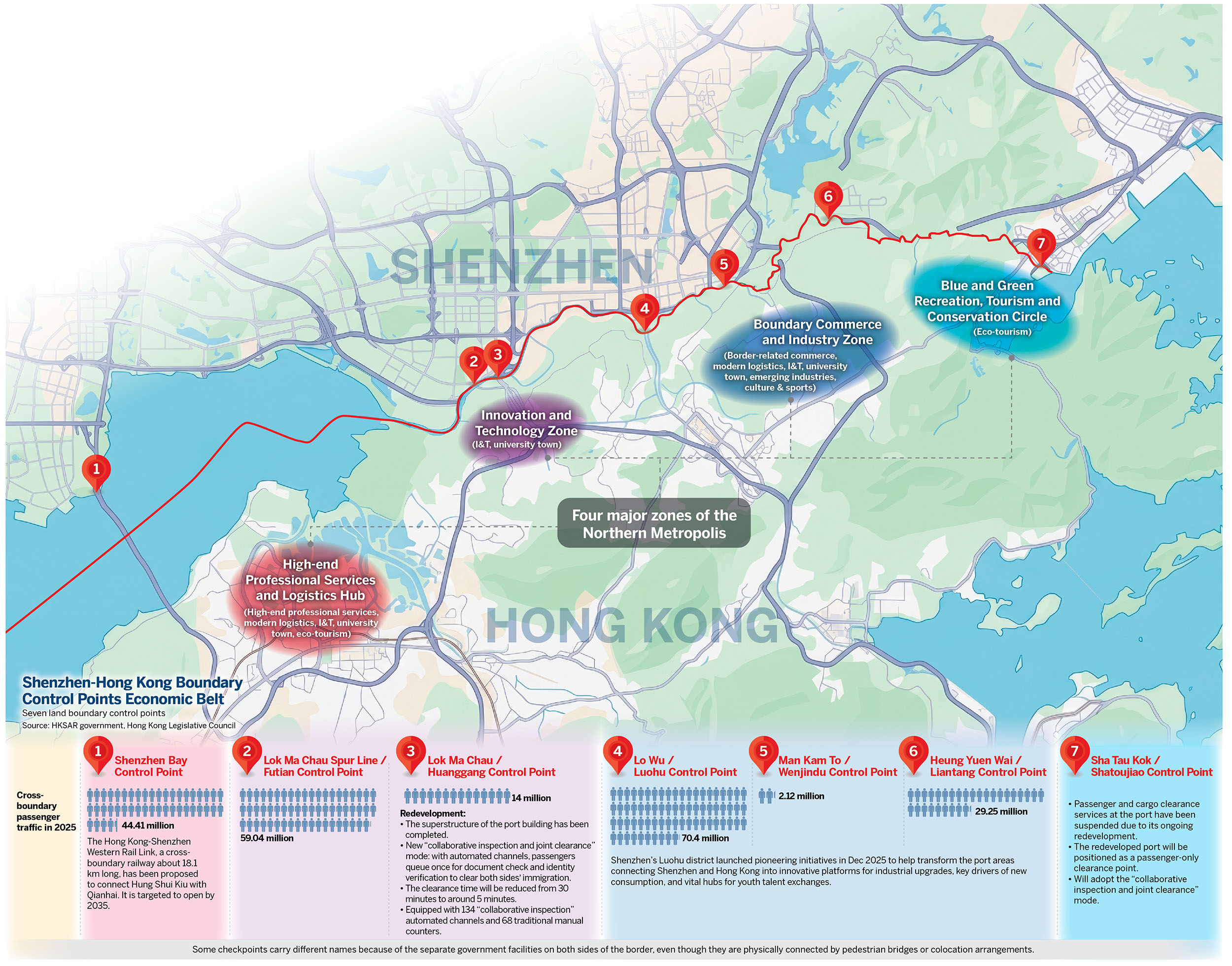

Editor’s note: As key transportation hubs in the Guangdong-Hong Kong-Macao Greater Bay Area, the cluster of ports in Shenzhen and Hong Kong is seeking a leap in value with a refreshed outlook and more integrated functions to turbocharge industries and the cities’ respective economies. China Daily presents a three-part series to document the transformation, with the first article spotlighting the significant potential of the land-port economic belt.

A chain of cross-boundary checkpoints has mushroomed on both sides of the Shenzhen River and its adjacent bay areas, carving out an economic corridor that serves as a key gateway for the flow of people, goods and capital between innovation epicenter Shenzhen and world financial hub Hong Kong.

After the twin cities’ ups and downs for almost half a century, the crossings are undergoing a profound transformation to enhance their value, aiming to convert massive traffic flows into fresh economic momentum.

Desperate for new development opportunities, Shenzhen and the Hong Kong Special Administrative Region have turned their sights to the boundary areas, with the southern Chinese mainland boomtown upgrading crossing facilities and integrating industries to further unleash the capabilities of the strategic passages, and the SAR spearheading its ambitious Northern Metropolis project to reshape the once-desolate area.

With greater development priorities, the future of this prime location is expected to be a strategic lever for both sides to address economic pain points, promote regional industrial upgrading and advance the country’s high-level opening-up.

The seven land-boundary crossings between Shenzhen and Hong Kong currently handle over 200 million passenger trips annually, accounting for 40 percent of the nation’s total inbound and outbound passenger traffic. They include the three busiest ports — Luohu, Futian and Shenzhen Bay — complemented by the only round-the-clock checkpoint, Huanggang, as well as Wenjindu, Liantang and Shatoujiao.

The figures speak for themselves. Cross-boundary visits at all ports hit a record high of 273 million last year, up 14 percent year-on-year, with an average of 750,000 movements logged daily. Since Hong Kong’s return to the motherland in 1997, passenger throughput between the two cities has more than tripled, and the trade volume is up 10 times to 790 billion yuan ($116 billion), magnified by the opening of more crossings.

“Linking two core cities of southern China and benefiting from the institutional advantages of ‘one country, two systems’, the Shenzhen-Hong Kong boundary area, driven by trade and innovation-technology industries, is of unique significance to the country,” says Xie Laifeng, who heads the Hong Kong, Macao and Regional Development unit at the China Development Institute.

“Whether it is in terms of passenger traffic or internationalization, it outperforms many other counterparts and even surpasses the economic vitality of some border regions between countries,” he says. “As cross-boundary traffic continues to rise, and integration of the Guangdong-Hong Kong-Macao Greater Bay Area enters a new phase, the boundary crossings’ functions need to be further upgraded, with new economic models in place to promote deeper industrial, livelihood and cultural connectivity.”

Pursuing such lofty goals, China has made extraordinary efforts to evolve ports of entry from peripheral passages to regional economic engines. Under the 14th Five-Year Plan (2021-25), the country added and expanded 40 boundary crossings, bringing the total to 311.

New phase, new plans

Entering the nation’s 15th Five-Year Plan period (2026-30), Shenzhen has made boosting the boundary area economy a key priority, pledging to adopt varied strategies for developing different land ports. The city’s renovated Huanggang Port is due to open this year, while Luohu, Shatoujiao and Wenjindu ports will be upgraded in the next few years, according to Wu Jun, director of the Cooperation and Development Division of the Office of Port of Entry and Exit of the Shenzhen Municipal People’s Government.

The upgraded checkpoints will see streamlined customs procedures, greater processing capacity and more clearly defined functions, Wu tells China Daily in an exclusive interview. The new-look Huanggang Port will release 500,000 square meters of land to back up the development of the Hetao Shenzhen-Hong Kong Science and Technology Innovation Cooperation Zone.

In the long term, Shenzhen may create a dedicated crossing in the Hetao cooperation zone to facilitate the movement of scientific researchers, as well as the Qianhai checkpoint of the planned Hong Kong-Shenzhen Western Rail Link — a vital cross-boundary infrastructure that will connect the two cities in just 15 minutes.

In Shenzhen’s push to strengthen the border crossings’ integration with industries, western checkpoints will focus on modern services and high-end consumption, while those in the central areas will facilitate the flow of scientific and technological resources, and those to the east will create new scenarios for cross-boundary consumption.

Luohu district — home to three checkpoints — took the lead in launching initiatives last year to revitalize the port economy, focusing on cross-boundary trade, high-end consumption, emerging technology applications and talent communication.

“Along with the earliest-developed crossings, Luohu has the closest ties, most frequent exchanges, and the most active cross-boundary consumption with Hong Kong,” says Liu Xiaomei of the Luohu District Development and Reform Bureau.

The city hopes to leverage these advantages and nearby industrial resources to introduce lightweight, high-value-added industries along the boundary, such as coordinating with Hong Kong in developing a life-and-health industrial park, exporting financial and knowledge services, and expanding the trade of fresh food and agricultural products, she says.

Boundary crossings are also excellent platforms for showcasing products and promoting the consumption of smart home devices, wearable technology, senior-friendly technology, automobiles, as well as gold and jewelry.

“Previously, the crossings mainly functioned as transit hubs — busy but underutilized. The initiatives are set to leverage their geographic advantages to make them destinations for Shenzhen and Hong Kong residents to work, live and relax,” Liu says.

On the other side of the boundary, the 300-square-kilometre Northern Metropolis is rapidly taking shape, and is on course to be Hong Kong’s most dynamic area in the next two to three decades. Its core industries — tech innovation, the digital economy, low altitude aviation and higher education — along with a projected population of 2.5 million and a new transport network centered on the Northern Link, are poised to fuel the region’s economic growth.

Zheng Yongnian, dean at the School of Public Policy of The Chinese University of Hong Kong, Shenzhen, says the “port economy” represents an upgrade from the traditional “transit economy”.

“By leveraging the traffic of boundary crossings, it fosters the development of local industries, such as consumption, trade and logistics, achieving an extension of industrial chains and economic value-added,” he said.

“A growing number of crossings are undergoing such transformation. Many countries are promoting economic growth, employment and trade by establishing free trade and special economic zones, or port clusters at seaports, land border crossings or airports, transforming them from economic outposts into hubs,” Zheng says.

Hong Kong business-sector lawmaker Erik Yim Kong has compiled an insightful research report in this field, saying the port economy holds promise as a new economic driver for Shenzhen and Hong Kong that will strengthen the overall level of openness and industrial competitiveness of the 11-city Greater Bay Area.

As natural conduits connecting both sides, the port areas can further explore opportunities in customs clearance facilitation, cross-boundary data flow, and mutual recognition of professional qualifications, providing valuable insights for other free trade zones and cross-border cooperation zones across the country.

Connecting domestic and international markets, developing border ports can further improve the efficiency of cross-boundary logistics, passenger and capital flow, backing the country’s “dual circulation” strategy and high-level opening-up, says Yim.

Tailored strategies needed

Given the varying levels of development in the border regions of both sides, different project strategies are essential.

Xie says that Shenzhen’s port cluster, having matured after years of development, demands new business models and greater internationalization to unlock its worth. He calls for urgent attention to enhance older ports with haphazard layouts, aging infrastructure and severe traffic congestion. For new ports being planned, allocating more space for new consumption formats and for innovation and entrepreneurship would be ideal.

With Hong Kong’s inno tech parks running at high capacity, the boundary port areas are well-positioned to absorb spillover demand. Attracting more Hong Kong and international firms to the area would also spur development of the Northern Metropolis, he says.

He said he believes Shenzhen’s crossings will see significant improvement under the 15th Five-Year Plan. With Luohu taking the lead, he hopes more areas will follow suit in scaling up port-driven economic development, pinning high hopes on Qianhai and Shekou in Nanshan district.

On the Hong Kong side, Yim says, developing the boundary areas has long been neglected, resulting in underdeveloped industries and inadequate supporting infrastructure. The authorities’ lengthy decision-making and implementation procedures have further slowed its pace of development.

He suggests forming a high-level Shenzhen-Hong Kong cooperation task force to elevate port development to the national level, jointly planned and developed by both sides to create complementary strengths. Hong Kong’s growth can be expedited through proposed dedicated legislation for the Northern Metropolis, which is set to innovate land development models and speed up project approvals.

In Zheng’s view, the port cluster should tap the SAR’s strengths to vigorously develop cross-boundary service industries — an area in which China’s economy has lagged and which is crucial to future international trade growth.

He advocates combining the policy advantages of both sides to make these checkpoints the first stop for companies going global. Building on the opportunities presented by the nation hosting this year’s Asia Pacific Economic Cooperation meetings in Shenzhen, the Shenzhen-Hong Kong port areas could further deepen policy openness on multiple fronts, including visa and tax-related measures, he added.

Zheng also recommends drawing on successful experiences of advanced port-economy models like Singapore, Dubai and Tokyo to develop diversified businesses at border ports, building free trade zones, and developing complete industrial chains in coordination with surrounding regions to ensure that the boundary corridor becomes an integral part of the national economy.

Next Actions

1. Elevating the strategic positioning of the border economic belt to a “national-level Shenzhen-Hong Kong cooperation platform”.

2. Jointly planning and developing the border region to achieve complementary advantages of the two sides.

3. Strengthening spatial planning for existing border crossings and strategically integrating them with high-value-added industries based on their respective strengths.

4. Reserving space for emerging industries, such as the low-altitude economy, as well as for innovation and entrepreneurship, when planning new border crossings.

5. Taking advantage of the nation’s hosting the 2026 Asia-Pacific Economic Cooperation meetings to deepen policies on opening up the boundary areas, particularly with regard to visa and taxation matters.

The fuel crisis across the global airline market is not only influencing passengers’ summer travel choices, but may also reshape the aviation industry’s international landscape, which is facing mounting challenges amid global turbulence.

The Guangdong-Hong Kong-Macao Greater Bay Area, which boasts multiple major airports, including an international air hub in Hong Kong, is also feeling the pinch. But the region’s relatively stable fuel supplies may help it fill the gap caused by international flight reductions and accelerate its development of a world-class airport cluster, experts say.

The soaring oil prices caused by conflict in the Middle East have driven up global jet fuel prices and led to supply shortages in many regions, resulting in widespread flight cancellations across international routes and increased fuel surcharges on airline tickets.

Jet fuel prices have reached a ten-year high. The domestic settlement price for jet fuel rose from 5,600 yuan ($821) per ton in March to about 9,800 yuan per ton in April, marking a monthly increase of 75 percent. International jet fuel prices have surged by more than 100 percent over the past two months, far outpacing the rise in crude oil prices.

The surge in prices is rapidly eroding profit margins, leading to the widespread cancellation of unprofitable routes. In April and May, which covers the Labor Day Golden Week, a large number of flights from Chinese mainland cities to Southeast Asia and Australia were canceled, including those to tourist hotspots such as Phuket, Bangkok, and Sydney.

In Hong Kong, Cathay Pacific and its subsidiary Hong Kong Express have canceled approximately 2 percent and 6 percent of their passenger flights, respectively, from mid-May through the end of June. Greater Bay Airlines has also canceled flights to Bangkok from May through September, as well as some flights to Taipei.

Zhou Shunbo, executive director of the New Economy Institute at the Shenzhen-based China Development Institute, said the fuel price surge has had a major impact on the operations of low-cost airlines, with larger airlines also being hit. Coupled with the Russia–Ukraine conflict, these geographic tensions have dealt another blow to the international aviation industry, which has been slowly recovering from the COVID-19 pandemic.

He believes that while some domestic travel demand may shift to high-speed rail, the uncertainty surrounding international flights and short-term price fluctuations will dent people’s willingness to travel abroad in the near term, particularly among budget travelers.

Reduced passenger flights will also cut cargo capacity in aircraft holds, which may drive up the shipping costs for goods that rely on air transport — such as precision electronic components and high-value seafood. This could further affect the development of core industries and everyday life in the Greater Bay Area, Zhou said.

If the situation persists, it may prompt national and local authorities to examine the long-term impact of rising fuel costs on urban development and to introduce policies to aid the aviation industry and its shift to sustainable energy.

He cautioned that flight slots at key international hubs — such as London Heathrow Airport — are highly valuable. If a carrier reduces its flights and gives up certain slots, they may be auctioned off to other airlines, making it difficult to re-enter that market.

Given the current ample supply of jet fuel in China, he believes the Greater Bay Area can seize this opportunity to capture market share from affected international markets and further the goal of developing its local airports into international aviation hubs.

Timothy Chui Ting-pong, executive director of the Hong Kong Tourism Association, said that in addition to the Labor Day holiday, the entire summer season from June to August is the peak season for tourism. Many students planning to study abroad will choose to fly from Hong Kong, and these plans will also be affected under the current circumstances, he added.

He said flight reductions would impact Hong Kong International Airport’s high-frequency, dense transit network as well as its cargo services — which rank first globally in terms of throughput — potentially weakening the city’s competitiveness as an international aviation hub in the long run. However, he emphasized that this is an industry-wide challenge troubling global airports.

Chui urged local airlines to maintain strategic routes connecting Hong Kong to Europe, Japan, the Chinese mainland and Australia, ensure a stable local fuel supply, and provide appropriate compensation to affected passengers to maintain their confidence in local services.

If the fuel crisis continues, the government should consider introducing support measures — for example, reducing fees for aircraft parking and airport operations, and providing subsidies for key trunk routes, he said.

As the Labor Day holiday approaches, many travelers have taken to social media to share their experiences of flight cancellations and discuss how to recoup their losses. Chen Xueqing, a traveler from Chongqing, booked a China Southern Airlines flight two months in advance to enjoy a vacation in Vietnam, which was subsequently canceled.

She had “carefully selected” the flight as it did not require her to take any extra leave. Like her, many people assumed that the wave of flight cancellations would only affect overseas aviation companies and did not expect domestic carriers to be affected as well.

Although she will receive a full refund, other flights on the same day had risen to 5,000 yuan, far exceeding the original cost of her ticket. Furthermore, she had already booked domestic flights and hotels in Vietnam, which were non-refundable, meaning she would incur a loss regardless of whether she went or not. She later negotiated with China Southern Airlines and managed to rebook onto an Air China flight on the same day.

To minimize potential losses, travelers are recommended to prioritize major airlines with a wide selection of routes and flights, carefully review the terms and conditions before purchasing international tickets, and opt for hotels and other travel products that offer free cancellation whenever possible.

Experts believe that retail magnate Richard Liu Qiangdong’s ambitious 5 billion yuan ($724 million) investment plan for the yacht industry, aiming to integrate the industry chain and expand the ecosystem, is set to give a significant boost to the fledgling yet promising market in the Guangdong-Hong Kong Macao Greater Bay Area.

The injection of capital and the nation’s policy tailwinds have led experts to advocate for related institutional reforms to fully invigorate the industry and stimulate the consumption vitality of the marine economy.

Liu, founder of China’s retail giant JD, launched the nautical brand Sea Expandary — a leading yacht project in China in terms of investment scale and industrial layout — on Feb 24. Dedicated to developing green and intelligent yachts, the venture will establish its headquarters in Shenzhen’s Qianhai area and a manufacturing base in Zhuhai.

By integrating the fragmented resources of the domestic yacht industry, the company will collaborate with the two coastal cities to enhance product technology, improve infrastructure construction and develop tourism routes, in a bid to establish a benchmark for the high-end yacht industry.

Hu Zhenyu, director of the Department of Sustainable Development and Blue Economy Research of China Development Institute, said he believes that the new brand will bring comprehensive advancement for the industry through technological iteration, industrial chain enhancement, and ecosystem expansion.

The company’s focus on green and intelligent solutions will accelerate the application of technologies such as new energy, smart navigation, and unmanned operations in the domestic yacht sector, driving industry transformation and enhancing international competitiveness, Hu said.

Its comprehensive industrial chain layout will attract supporting industries like the manufacturing of core components, maintenance and repairs, and financial services.

Furthermore, the project is expected to drive the development of infrastructure such as public berths and green refueling stations, while fostering crew training, secondhand transactions and the leasing of vessels, addressing key bottlenecks in developing yacht tourism and related consumption, said Hu.

As an integration of the manufacturing and service industries, the yacht industry can also expand consumption scenarios in the Greater Bay Area's marine economy, promoting the transition of marine engineering equipment toward lightweight and intelligent designs, he added.

Louis Liu Yi, professor at the School of Tourism Management at Sun Yat-sen University, said that the Greater Bay Area's yacht market has lacked the participation of influential business figures in recent years, and earlier investments by Hong Kong tycoon Henry Fok Ying-tung’s family have not yielded significant development.

Richard Liu’s involvement instills great confidence in the market, and the company’s vision has brought new hope for the Greater Bay Area’s yacht sector to enhance its influence.

He hopes that this initiative will enhance the value of the local yacht industry, promote the application of innovative technologies, and stimulate consumption in supporting services.

Jerry Ye Jialin, vice-president of Guangdong Yacht Tourism Association, highlighted the industry’s vast market potential. In a press conference held in December, China’s Vice-Minister of Transport Li Yang said the ministry is drafting measures to boost yacht consumption, a new growth point in the coming years.

Over the past three years, the annual growth rate of newly registered yachts in China has exceeded 40 percent, shifting toward mass-market scaled development, according to Li.

Calling for institutional improvements to capitalize on the trend, Ye urged local governments to enhance the management of yachts and public marinas, streamline procedures for Hong Kong yachts traveling to Shenzhen, and permit their visits to more Greater Bay Area cities.

“The aim is to systematically lower the costs associated with yacht ownership and usage, enabling more people to embrace the new lifestyle and consumption pattern,” said Ye.

In a gradual revolution of public parenting spaces, a new facility -- the "Father-and-Baby Room" is popping up in shopping malls across Chinese cities, signaling a shift toward a more equitable distribution of childcare responsibilities.

At a shopping center in the south Chinese metropolis of Shenzhen, the "super daddy zone" is easily identifiable by a glowing blue bottle logo.

Soundproof magnetic doors ensure privacy, while illustrated guides on the walls demonstrate how to prepare formula and hold an infant. Fathers are often spotted pushing strollers to take care of their babies in this space.

Nearby, a "Men's Parenting Room" sits beside a "Women's Parenting Room" at another mall in Shenzhen, both equally equipped with diaper-changing stations, sinks with hot and cold water, and formula-preparing areas.

"To meet customers' needs, we've set up such baby care rooms for both dads and moms on two different floors. It encourages fathers to be more involved in taking care of the baby," a mall staff member explained.

The key difference from traditional mother-and-baby rooms is the omission of private breastfeeding cubicles, focusing just on care, feeding, and rest functions. A more inclusive and practical trend, however, is merging the two into gender-neutral "family nursing rooms."

Some establishments have re-branded the previous "Mother-and-Baby Rooms" as simply "Nursing Rooms," with clear zoning to separate breastfeeding areas from open washing and changing spaces. This allows fathers to assist with childcare while respecting the privacy of nursing mothers.

Liu Xiao, a father who just changed his one-year-old daughter's diaper in one such room, expressed his approval for this space. "These facilities are very user-friendly and convenient. They actually influence our choice of where to shop," he said. "I believe the traditional idea that 'men work outside, women manage the home' is fading. Fathers should join in parenting. My daughter is very attached to me, and I find it very rewarding."

This evolution mirrors profound changes in Chinese families' parenting concepts, said Ming Liang, executive director of the Department of Urbanization of China Development Institute, adding that such changes have reshaped fathers' role in parenting and pushed society toward a more balanced model of shared parenting.

Traditionally, public parenting facilities in China were almost exclusively "Mother-and-Baby Rooms," designed to protect the privacy of breastfeeding women, often accompanied by "No Men Allowed" signs.

However, as societal norms shift and family structures evolve, fathers are taking a more active role in child-rearing, particularly among the "post-90s" and "post-95s" generations who are now the primary childbearing demographic. This growing desire for shared responsibility has clashed with the reality of available facilities, according to Ming.

Experts believe that the emergence of father-and-baby rooms fills this gap. Building a fertility-friendly society requires multi-dimensional support policies to ease family burdens and promote shared parenting.

The transition from "Mother-and-Baby" to "Father-and-Baby" or just "Nursing" rooms signifies more than a name change. It marks a profound step in social progress, said Ming.

Hong Kong remained in third place in the global ranking of financial centers, following New York City and London, according to the latest Global Financial Centers Index.

Despite the impact of the COVID-19 pandemic, Hong Kong scored 715 points, only one point less than its previous ranking half a year earlier. List-topper New York lost three points to score 759, while London came in second, dropping 14 points to 726.

The GFCI was jointly published on Thursday by the China Development Institute, a Shenzhen-based think tank, and London-based think tank Z/Yen.

ALSO READ: HKSAR still a global finance center, magnet for international investors

The gap between Hong Kong and the two top Western financial centers is narrowing, said Yu Lingqu, vice-director of the Center for Financial Studies at the China Development Institute.

The semiannual ranking bases its results on the study of five areas — business environment, human capital, infrastructure, financial sector development, and reputation. The list ranked 126 financial centers worldwide.

Among the subindexes, Hong Kong ranked third in reputation globally. In the aspects of business environment, human capital, and infrastructure, the city grabbed fourth place. In financial sector development, Hong Kong ranked 11th.

Yu said financial centers on the Chinese mainland generally performed well in financial technology and reputation. “Financial industry professionals across the world are upbeat over the outlook of Chinese financial industry, believing that there is large potential for growth,” he said.

ALSO READ: ‘HK's status as global financial hub intact amid pandemic’

But he added that mainland financial centers are stronger in “hard power” than in “soft power”.

“They needs to learn from Hong Kong’s experience to further enhance their financial ‘soft power’, including business environment, human capital and infrastructure,” Yu said.

The researcher also said that the findings of the latest ranking was based on the data collected as of the end of 2021 and did not reflect the recent changes in the world’s financial situation, including the Omicron outbreak, the Russia-Ukraine conflict, and the US Federal Reserve’s interest rate hike.

“Global financial centers are facing a number of uncertainties. We need to improve risk management, create a sound business environment and strengthen cooperation between financial centers to promote better growth of the world economy,” Yu said.

READ MORE: PBOC support for HK's financial hub status solid

Shanghai ranked fourth in the GFCI, advancing two places from the previous ranking. Beijing and Shenzhen also made into the top 10 list, ranking the eighth and 10th respectively.

Los Angeles was fifth, followed by Singapore and San Francisco. Tokyo took the ninth place.

China and Japan have large room for cooperation in emerging industries and the two sides should seek complementary development, scholars said on Thursday.

They made the remarks at an online seminar on China-Japan industrial cooperation and development, co-organized by the Shenzhen-based think tank China Development Institute and Beijing-based think tank Pangoal Institution.

"For China and Japan, the space for cooperation in traditional industries is not that large. But in emerging industries, it is huge," said He Jun, director of the enterprise innovation research office of the Institute of Industrial Economies at the Chinese Academy of Social Sciences.

"This is because each of the two countries has developed unique advantages in emerging industries. Therefore, they can leverage each other's strengths to jointly promote the development of those industries."

He took the industrial internet as an example. "While Japan excels in software and operational technology, China is developed in communication technology. If the two could work together to form a sound cooperative mechanism, it will be a win-win situation for both sides."

He's view was echoed by Cao Zhongxiong, director of the New Economy Research Centre at CDI, who believes China and Japan could explore more cooperation in blue ocean markets in the digital field by integrating China's digital technologies with Japan's manufacturing.

Japan can also provide talent support for the development of the Chinese digital economy, he added.

Cao also noted that China's globalization drive, transformation of industrial structure and consumption upgrade will create large opportunities for Japan and called on Japan to grasp the opportunities.

The list of the top global financial from Z/Yen in London shows a continued shift to the Asia and some sharp movement, perhaps Brexit-related, to among some of the British off-shore centers. Released twice a year since 2007, the Global Financial Centres Index (GFCI) has since 2016 been a collaboration between Z/Yen, a London think tank, and the China Development Institute, a national think tank focused on public policy.

The Index started with a focus on four leading financial centers — London, New York, Paris and Frankfurt, recalled Michael Mainelli, executive chairman of the Z/Yen Group XX. It now includes 100 financial centers.

“When 60% of an index moves from Western centres to Asian centres in a decade, it is a time for reflection,” wrote Mainelli.”Some of the shifts have been geopolitical, ranging from the increasing economic importance of China, to global conflicts, sanctions, trade flows, financial crises, and demography. Other shifts have been deliberate and intentional policies directed at increasing the attractiveness of specific financial centres for relocation and inward investment.”

London and New York jostle for first place, as they have for year, with New York on top this time. Both fell slightly in the ratings and Hong Kong is only three points behind London and Shanghai overtook Tokyo to move into fifth place while Beijing, Zurich and Frankfurt moved into the top ten, replacing Toronto, Boston and San Francisco. It is likely that an Asian center will have the top slot very soon, Mainelli added.

Some smaller Chinese cities are rising in importance — Hangzhou was added to the list with this report. An investment banker based in New York commented “We all know about Hong Kong and Shanghai but a number of secondary Chinese centres are appearing on the radar now.”

Cities that are newcomers to the list might be surprised to learn what they can do to attract the sort of highly educated professionals that a financial center needs. Mercer, the consultancy, recently commissioned a study which surveyed 7,200 workers and 577 employers across 15 emerging megacities in seven countries.

Mercer sees some of the cities that Z/Yen identified as part of a larger trend.

“In 10 years, nearly half of all economic growth will originate from just 400 cities and the one billion residents who call them home. That’s why business leaders and city officials need to be more creative in the fight for talent in the U.S. and abroad. To develop tactics for recruiting and retention, leaders first must understand the unique needs of tomorrow’s workforce,” the company said in describing its survey results.

David Anderson, president, international at Mercer, said businesses need to understand their audience.

“It’s cliché but in business, the customer is always right. Yet when it comes to people management strategies, employers rarely listen to their workforce – and that must change. Call it Business to the Individual, or B2I – there isn’t a one-size-fits-all solution for communicating with employees. Future leaning companies will employ customizable, personalized recruiting and internal communications strategies to be effective.”

Mercer sees people remaining at the center of evolving technologies like automation, AI and robotics. But they have different expectations of the impact of technology — 24% of employers expect individuals will be replaced by technology while only 14% of workers feel that way. The company says companies must be transparent about skills which may be phased out. Several other studies have said that as some processes become automated, companies will increasingly value soft skills such as communications and empathy.

When it comes to designing urban neighborhoods that will be attractive, the study found a few surprises. Supermarkets or shopping centers placed high at 77%, followed closely by being close to a bank branch, at 72%. Really? Aren’t branches supposed to be obsolete? Convenient transportation ranked with 66% of respondents, schools for children at 59% while parks and green space were just 46% and convenient pools or gyms 37%.

The study could be useful reading for emerging financial centers.

For GFCI 24, the group researched 110 financial centers and added four new ones — Cape Town, GIFT City (Gujarat), Hangzhou and Sofia. Brexit may have been behind the moves up by Zurich, Frankfurt, Amsterdam, Vienna and Milan while off-shore British Crown dependencies Jersey and Guernsey with the Isle of Man tumbling 27 places. Bermuda on the other hand rose six places to Number 30.

The report said that Brexit continues to be a major source of uncertainty for many centers with some respondents asking if London would retain its critical mass after Brexit. Respondents in London are less optimistic than those in other centres, reflecting the uncertainty over Brexit, the report said.

”Getting very fed up with Brexit,” commended a pension fund manager in London. “We cannot continue to operate with so much uncertainty. Many of the staff here are trying to plan for their futures.”

UK and USA respondent were also concerned about restriction in movement of talented staff. Regarding infrastructure, bankers wondered how to foster a FinTech environment and also cited a need for better air travel connectivity from some centers.

“Air travel infrastructure and having direct flights into and out of centres is becoming ever more important,” said an investment professional in Seoul.

Showing significant gains were Astana, the capital of Kazakhstan, Budapest, St. Petersburg and Tallinn while Cyprus and Warsaw fell, and Sophia was a new entrant tot he index. Dubai, Abu Dhabi and Doha all rose significantly, reversing the trend from GCFI 23.

Western Europe’s leadership position has been under challenge for several years as the assessment of the top five centers in Asia/Pacific and North America have improved, overtaking western Europe.

Chinese centers continue to exhibit strength as Shanghai passes Tokyo to enter the top five and Kong Kong, Singapore and Shanghai continue to close the gap on the leaders, the report said, adding a comment from a commercial banker based in Paris: New York and London don’t seem to be doing anything to fight off the Asian challenge.”

China will invest CNY 474.1 billion (US$67.9 billion) to improve rail connection in the Greater Bay Area, building 775 km (480 miles) of intercity railway and five transport hubs, according to a plan approved by the National Development and Reform Commission (NDRC).

The Greater Bay Area is an ambitious scheme announced by the Chinese government in 2017 to link Hong Kong, Macao and nine cities in Guangdong province to form an integrated mega economic and technology hub capable of rivalling San Francisco’s Silicon Valley, writes South China Morning Post.

In recent years the scheme has been gradually rolled out with the construction of the Hong Kong-Zhuhai-Macao Bridge and the Hong Kong-Guangzhou high-speed train, as well as inter-region cooperation on other infrastructure projects, education and scientific research.

The connectivity programme, which was approved on 30 July by the NDRC, China’s top economic planning agency, is intended to cover all cities in the area above county level with 5,700 km of railway by 2035. By then, passengers would be able to commute between major cities in the Greater Bay Area within an hour, major cities to smaller cities within two hours, and major cities to capitals in surrounding provinces within three hours, according to the plan.

Under the scheme, transport hubs will be built within cities, connecting airports, train stations and linking intercity rail systems with inner city transport. Hong Kong and Macao would also be better integrated into the regional grid, the plan said.

Currently, connectivity was limited in the region, said Guo Wanda, executive vice-president of the China Development Institute, a Shenzhen-based think tank.

“There are still too few [railway] lines between cities, it’s inconvenient to switch from railways to subways and other services [in different cities] – including ticketing and road signs – are not integrated,” he said.

Under the new plan, small and medium-sized cities would be better connected, instead of being overshadowed by major cities, said HuoWeidong, who has a doctorate from the Institute of Guangdong, Hong Kong and Macao Development Studies at the Sun Yat-sen University in Guangzhou.

In addition, Huo described the new plan as a “breakthrough in design” because it would consider intercity connection as a “hub-to-hub” concept compared with the old “city-to-city” model, easing the movement of people, business and goods.

“The hub-to-hub design will also strengthen the connection of major airports and small and medium-sized cities, and I am confident that this will present opportunities attractive to overseas investors,” he said.

Immediate effects of the plan included boosting the economy within the Greater Bay Area, said Peng Peng, executive director of the Guangdong System Reform Research Society.

“Guangdong, the largest province in terms of foreign trade [in China], has been hit hard by the coronavirus pandemic and [the souring of] US-China relations. We can’t depend on foreign trade for the recovery,” he said. “In the short term, the room for boosting domestic demand will be limited. So infrastructure construction will be the main avenue for growth.”

However there were difficulties in carrying out the plan, such as financing, Peng said.

“Guangzhou’s financial situation is [less robust than] Shenzhen’s. A critical factor [for this project] is whether local governments can arrange the financing smoothly,” he said.

Shenzhen firms hike investment in R&D sector

Nearly 20 percent of Shenzhen-registered listed companies devoted more than 10 percent of their operating revenue to research and development last year, a level on par with globally leading high-tech enterprises like Google and Apple, according to a report.

In all, 256 companies covered in the Shenzhen-registered Listed Companies Development Report disclosed their R&D spending in their 2017 annual reports.

Between them, the companies spent approximately 77.75 billion yuan ($11.19 billion) on R&D, up 24.8 percent year-on-year.

Their average R&D intensity - the ratio of R&D spending to operating revenue - was 3.95 percent, up 0.24 percentage points year-on-year, the report said.

A total of 45 listed companies, or 17.6 percent, poured more than 10 percent of their operating revenue into R&D in 2017.

The report, published in Shenzhen on Tuesday, was jointly compiled by the Shenzhen-based think tank China Development Institute and Hongxin Securities.

Researchers based their findings on 27 indicators in four main areas - scale, development potential, business capacity and social contribution.

"The figures show that Shenzhen-registered listed companies are making great efforts on enhancing their innovative capability," said Yu Lingqu, a researcher from CDI.

"A 10 percent R&D intensity means they are on the same level as technology giants such as Google and Apple."

According to the report, information technology was the sector that took the lead. Of the 10 listed companies with the biggest R&D investment, eight were IT companies.

The R&D investment of Tencent Holdings Ltd, the world's largest game maker and second biggest social media firm by revenue, and telecom equipment maker ZTE Corporation amounted to over 10 billion yuan, respectively.

As of the end of 2017, the number of Shenzhen-registered listed companies had reached 367, with a market capitalization amounting to nearly 10.3 trillion yuan.

In 2017 alone, 46 Shenzhen enterprises made their initial public offerings in domestic and international capital markets.

Information technology and finance were the two sectors with the largest market capitalization, combining to make up over 70 percent of the total.

"This shows Shenzhen's economic growth is driven by technology and finance," Yu said.

In 2017, Shenzhen-registered listed companies generated approximately 4.07 trillion yuan in operating revenue, growing 20.8 percent from a year earlier.

Of the total 367 Shenzhen-registered listed companies, the report covered 341. The rest were excluded either because their stocks were suspended from trading for a long time, or they had not published their annual reports by the end of June.

After years of booming growth, China’s real estate sector, a major pillar of the world’s second-largest economy, is wobbling.

The fundamentals of China’s real estate market will face “a year of recession” in 2019, China International Capital Corp. (CICC) said Monday in a research report. Sales, investments and new construction starts will decline significantly next year, according to researchers at the largest state-backed investment bank in China. In response, the government should alter policies that were put in place to cool the market, the researchers said.

The assessment reflects the chill in the market that Chinese property developers have already begun to feel, prompting them to dial back land purchases. Growth in China’s real estate investment slowed to 8.9% in September from 9.2% in August, and home sales by floor area fell 3.6% from a year earlier, the first time since April.

During the ordinarily golden September-October property-sales season, slack demand forced developers to offer huge promotions, including free cars and lower down payments. Some developers slashed prices as much as 30%, angering earlier buyers who paid higher prices.

The central government initiated a campaign to control surging property prices in September 2016. Based on previous cycles, policymakers usually begin to relax tightening measures after housing sales have declined for six months. Based on that, CICC projected that the next round of policy easing may come at the end of the 2019 first quarter or the start of the second quarter.

But as China’s economy faces broader headwinds and uncertainty from an intensifying trade war with the United States, CICC’s researchers recommend an earlier policy adjustment. China’s top financial and economic officials haven’t addressed the cooling outlook for the property market.

According to the CICC assessment, property sales across China are likely to fall for the first time in five years, with sales by floor area and by prices both expected to decline 10%. The downward pressure on home sales and prices will be especially obvious in third- and fourth-tier cities, while the property market in the first- and second-tier cities is expected to be resilient.

CICC said it expects real estate investments in 2019 to decline by 5% and new construction starts, by 10%, reflecting weakening fundamentals in the property industry.

China Vanke Co. Ltd., one the country’s biggest developers, recently said "survival" was the ultimate goal for the next three years as a “turning point” has arrived for the industry.

The Mid-Autumn festival and the week-long National Day holiday normally bring buyers out in masses in September and October, spurring residential property sales. But this year has been different, even for the country's biggest developers.

During the weeklong public holiday at the start of October, sales in 31 cities fell 27% from a year earlier, according to Shanghai-based property consultant CRIC.

Several major Chinese property developers significantly slowed their land purchases in September.

A total of 2,332 plots of land, with a gross area of 97.3 million square meters, were available for sale in September, according to a China Index Academy report. That was an 8% decrease year-on-year. A total of 1,950 plots were sold, down 13% compared with the same period last year.

The CICC report suggests four feasible paths for policy adjustment next year, including increasing supply, lowering the down payment ratio, relaxing excessive restrictions on mortgage interest rates and increasing the amount of mortgage loans.

Measures to control housing prices could be maintained, but pricing mechanisms and price tracking management should be improved, the researchers suggest.

On the outlook for property stocks, CICC said it thinks the P/E ratios of mainland listed A stocks and Hong Kong-listed H stocks are at a historic low level. Even though a sales decline will raise concerns about property developers’ sales and profit growth in the short term, the negative effects are likely to be far less than the boost expected from policy adjustment, the bank said.

Beijing and Washington are unlikely to reach a deal on intellectual property rights or further opening up of China’s financial market – even if the leaders of the two countries meet later this month, a key Chinese government adviser said.

“What they were negotiating in Beijing and Washington in the past round [of talks earlier this year] was mostly about trade itself,” Fan Gang, a former member of the monetary policy committee of the People’s Bank of China, said in a speech at Harvard University on Wednesday.

Since the countries had not even begun to discuss the two issues at the heart of the trade war, it was “hard to have a solution” to the dispute, Fan said.

When asked whether China would improve its intellectual property protection and further open up its financial market to ease trade tensions with Washington, Fan said the reforms were necessary but would not come quickly.

“The reforms may change the position of the other side, but it will take some time. It’s not a short-term issue. It’s a midterm issue,” Fan said.

Chinese President Xi Jinping is expected to meet his US counterpart Donald Trump on the sidelines of the G20 summit in Buenos Aires at the end of this month.

They are not talking about trade … Buying doesn’t solve the problem

Fan Gang

Analysts on both sides have expressed confidence recently that Beijing and Washington might reach a truce over the trade dispute during the summit, in the two leaders’ first meeting since a tit-for-tat trade war between their nations broke out in July.

But Fan, a leader in an economists’ club founded by Chinese Vice-Premier Liu He, said he was pessimistic about bilateral ties “in the short-run and the long run”. Liu had led several rounds of trade negotiations this year with Trump administration officials including Treasury Secretary Steven Mnuchin.

“I don’t think in the short-run you can reach an agreement,” Fan said. “How can you reach agreements with Donald Trump and his team? They are not talking about trade. How much can China actually buy? Buying doesn’t solve the problem.”

The economist said he expected the ideological conflicts from the trade war to last.

“It’s about internet control, it’s about ideology, it’s about national security and so-called political superiority,” he said. “In the long run, it’s hard to have a solution.”

I think the United States is united on China

Fan Gang

Fan also acknowledged the consensus on China’s trade practice across the US political spectrum.

“It was the [US midterm] election day yesterday and anything seems to be a controversy, but I think the United States is united on China,” he said.

His comments came as Washington continued to express concern about China’s ambitious manufacturing plan, “Made in China 2025”, which channels state funds to domestic companies developing advanced technologies in robotics, telecommunications and aviation.

The initiative, which aims to break China’s reliance on foreign technology and pull its hi-tech industries up to Western levels, has become a lightning rod for Washington’s – and Trump’s – ire in the trade war with Beijing.

In a post-midterm-election address on Wednesday, Trump called Made in China 2025 “insulting” and suggested Beijing was backing away from it.

Fan stressed that continuing the initiative was beyond question.

Nevertheless, his views reflected a school of thought within Beijing that boldly favours China and the United States reaching a compromise to reduce the intensity of the trade tensions. He said the trade war had accelerated China’s long-needed market reform.

“There are so many things that the Chinese central leadership has agreed to do, committed to doing, but didn’t do for such a long time,” Fan said. “After the trade war, a lot of things started moving.”

Beijing and Washington are unlikely to reach a deal on intellectual property rights or further opening up of China’s financial market – even if the leaders of the two countries meet later this month, a key Chinese government adviser said.

“What they were negotiating in Beijing and Washington in the past round [of talks earlier this year] was mostly about trade itself,” Fan Gang, a former member of the monetary policy committee of the People’s Bank of China, said in a speech at Harvard University on Wednesday.

Since the countries had not even begun to discuss the two issues at the heart of the trade war, it was “hard to have a solution” to the dispute, Fan said.

When asked whether China would improve its intellectual property protection and further open up its financial market to ease trade tensions with Washington, Fan said the reforms were necessary but would not come quickly.

“The reforms may change the position of the other side, but it will take some time. It’s not a short-term issue. It’s a midterm issue,” Fan said.

Chinese President Xi Jinping is expected to meet his US counterpart Donald Trump on the sidelines of the G20 summit in Buenos Aires at the end of this month.

Analysts on both sides have expressed confidence recently that Beijing and Washington might reach a truce over the trade dispute during the summit, in the two leaders’ first meeting since a tit-for-tat trade war between their nations broke out in July.

But Fan, a leader in an economists’ club founded by Chinese Vice-Premier Liu He, said he was pessimistic about bilateral ties “in the short-run and the long run”. Liu had led several rounds of trade negotiations this year with Trump administration officials including Treasury Secretary Steven Mnuchin.

“I don’t think in the short-run you can reach an agreement,” Fan said. “How can you reach agreements with Donald Trump and his team? They are not talking about trade. How much can China actually buy? Buying doesn’t solve the problem.”

The economist said he expected the ideological conflicts from the trade war to last.

“It’s about internet control, it’s about ideology, it’s about national security and so-called political superiority,” he said. “In the long run, it’s hard to have a solution.”

Fan also acknowledged the consensus on China’s trade practice across the US political spectrum.

“It was the [US midterm] election day yesterday and anything seems to be a controversy, but I think the United States is united on China,” he said.

His comments came as Washington continued to express concern about China’s ambitious manufacturing plan, “Made in China 2025”, which channels state funds to domestic companies developing advanced technologies in robotics, telecommunications and aviation.

The initiative, which aims to break China’s reliance on foreign technology and pull its hi-tech industries up to Western levels, has become a lightning rod for Washington’s – and Trump’s – ire in the trade war with Beijing.

In a post-midterm-election address on Wednesday, Trump called Made in China 2025 “insulting” and suggested Beijing was backing away from it.

Fan stressed that continuing the initiative was beyond question.

Nevertheless, his views reflected a school of thought within Beijing that boldly favours China and the United States reaching a compromise to reduce the intensity of the trade tensions. He said the trade war had accelerated China’s long-needed market reform.

“There are so many things that the Chinese central leadership has agreed to do, committed to doing, but didn’t do for such a long time,” Fan said. “After the trade war, a lot of things started moving.”

He cited China’s lifting of ownership limits for foreign car firms in April, which enticed US carmaker Tesla to build a plant in Shanghai; a further opening of the Chinese financial market; and lowering of tariffs as examples of trade war-impelled changes that have happened in recent months.

Other Washington policymakers, including Danny Russel, a former assistant secretary of state for East Asian and Pacific affairs, agreed that any deal between Trump and Xi at G20 would be limited or incremental if at all.

He said the Trump administration had publicly aired “such a list of offences by China, that are shared not only by the business community or the policy community but by Congress, that it may be hard for the administration to simply set those issues aside and say, ‘We’ve reached a deal on the trade figures, but we haven’t dealt with forced transfer of technology, of cybertheft, of intellectual policy, of the industrial policy of Made in China 2025’”.

Russel made his remarks at an Asia Society round table discussion in New York on Wednesday.

“If you don’t have a very clear direction of where to go, you confused the ministries and people who implement the policies,” Fan said of the central leadership’s shifting position on market reforms.

“You can’t blame all the problems on lower level bureaucrats,” he said. “That’s why I called the trade war a wake-up call.”

A fierce debate is raging about the future of China’s economy. Many believe it is being held behind closed doors at the powerful Politburo.

They would be wrong. Instead, these discussions are taking place in the hallow halls of Peking University.

In the past three weeks, Zhang Weiying, the prominent liberal economist and a professor at the prestigious seat of learning in Beijing, has mapped out his vision of the future.

On Monday, Fan Gang, another influential professor at Peking University and president of the China Development Institute, outlined a similar roadmap.

Their views come at a time when the world’s second-largest economy is being buffeted by internal and external headwinds, including rising trade tensions with the United States.

Zhang has attributed the Cold War-style stand-off between Beijing and Washington to China’s flawed economic model.

“Domestically, misleading yourself means a future of self-destruction,” he said in a speech, which appeared on the National School of Development’s website before it was taken down by the authorities.

“Blindly emphasizing the unique Chinese model means going down the road of strengthening state-owned enterprises, expanding government power, and relying on industrial policy. This will lead to a reversal of the reform process, the abandonment of our predecessors’ great cause of reform, and ultimately economic stagnation,” he continued.

“Externally, misleading the world leads to confrontation. From the Western perspective, the ‘China model’ theory makes China into an alarming outlier, and must lead to conflict between China and the Western world,” Zhang added.

During the past six months, international relations with the West have deteriorated as quickly as the economy.

Threatened

Tariffs worth more than US$250 billion have already been slapped on Chinese exports to the US by President Donald Trump.

He has also threatened to impose duties on the remaining goods and products worth another $258 billion, citing “unfair practices” and “intellectual property violations.”

Moreover, the fallout has rippled across the entire economy with GDP growth falling to levels not seen since the Great Recession of 2009, while consumer spending has slowed and factory activity has dropped.

“China is serious about liberalizing its economy and its pace of doing so has been accelerated by the trade war with the United States,” Fan, who is also an adviser for President Xi Jinping’s government, said.

“That kind of willingness is genuine … China recognizes that it needs more liberalization to become more competitive in the global market.”

But the pace of reforms is in danger of stalling with “vast interest groups” lobbying against further opening up to overseas competition.

This, he pointed out, had to change as China’s economy goes through a transformation from low-cost manufacturing to high-tech production, backed up by a thriving services industry and a more sophisticated consumer sector.

“China should move on,” Fan said. “You have more and more companies operating internationally and enjoying international terms for competition. Why do you still have those protections? More and more companies don’t need it.

“Previously, China’s pressure came from the top. The policymakers put pressure on the localities, on the companies, to push them to change. [Now,] some outside pressure [such as the trade dispute] may serve as a good push.”

Realigning the economy and being embroiled in a brawl with the US has prompted the Politburo, which is the main decision-making body of the ruling Communist Party, to reiterate its pledge to stimulate growth.

So far, the government has unveiled a raft of measures, including tax cuts, infrastructure spending and cheap financing for struggling private sector companies, while pressing ahead with its clampdown on debt.

A stimulus-inspired package for the markets has also been rolled out after nearly $3 trillion was wiped off the Shanghai Composite Index and $1.1 trillion off Shenzhen in the past nine months. This, in turn, has hit the spending power of more than 150 million middle-class investors.

Priority

Boosting confidence has become a priority with the Politburo admitting on Wednesday that “downward pressure on the economy has increased” and that “timely measures” must be taken, without revealing concrete proposals.

Hours later, Chinese factory activity statistics for small- and medium-sized companies were released.

The numbers were disappointing with the Caixin Purchasing Managers’ Index, or PMI, edging up slightly higher to 50.1 from 50.0 in September while remaining in expansion territory.

“China’s economy has not seen obvious improvement,” Zhengsheng Zhong, the director of macroeconomic analysis at CEBM Group, a Caixin subsidiary, said.

“Overall, expansion across the manufacturing sector was still weak. Production and business confidence continued to cool despite stable demand. The pressure on production costs didn’t ease,” he added.

Roughly 24 hours earlier, the official PMI, compiled by National Bureau of Statistics, revealed that manufacturing growth was at its weakest level in more than two years, fueling concerns about the aftershocks of tit-for-tat tariffs and a perceived slowdown in major reforms.

“China’s reform and opening-up and the China-US strategic cooperation are two inter-related things,” Sheng Hong, the executive director of the Unirule Institute, an independent Chinese think tank, said. “That is to say, there is no strategic cooperation without reform and opening-up, nor is there reform and opening up without China-US strategic cooperation.

“Today, China faces the risk of leaving the path of reform and opening up, which would risk the loss of strategic cooperative relations with the US. Such a result would be a complete failure.”

Amid the carnage of the trade battle, the great China debate continues.

BANGKOK - China is serious about liberalising its economy and its pace of doing so has been accelerated by its trade war with the United States, says Chinese economist and government adviser Fan Gang.

"That kind of willingness is genuine… China recognises that it needs more liberalisation to become more competitive in the global market," said the Peking University professor and president of Shenzhen-based think-tank China Development Institute.

But the pace of reforms has been hampered by what he called "vast interest groups" lobbying Beijing against lifting the protection for local firms that it has maintained for years as a developing country.

"China should move on. You have more and more companies operating internationally and enjoying international terms for competition. Why do you still have those protections?... More and more companies don't need it," Professor Fan said, referring to Chinese companies like mobile phone maker Huawei.

"Previously, China's pressure came from the top. The policymakers put pressure on the localities, on the companies, to push them to change," he said. Now, "some outside pressure may serve as a good push".

Prof Fan was speaking to The Straits Times on Tuesday (Oct 30) on the sidelines of the Forbes Global CEO Conference in Bangkok.

Global stock markets have taken a bumpy ride this year after US President Donald Trump triggered a trade war between the world's two largest economies, accusing China of stealing intellectual property and unfair trade barriers.

A series of tit-for-tat measures has resulted in more than US$250 billion (S$346 billion) worth of Chinese goods subject to tariffs of up to 25 per cent in the US, and some US$110 billion worth of US goods are subject to reciprocal taxes in China.

Analysts expect the trade war to put a drag on global economic growth.

Mr Trump and Chinese President Xi Jinping are expected to meet on the sidelines of the Group of 20 (G-20) summit in Buenos Aires next month.

Mr Trump, while saying he expects to make a "great deal" with China, has warned that he is ready to slap tariffs on even more products if a deal does not transpire.

In the face of the trade war, China should focus on developing its own market rather than retaliation, said Prof Fan.

"As long as you can really extend your market further, as long as you can attract more investment in your industrial supply chain, you can win," he said.

Asked if he was concerned that companies which export products to the US may relocate from China to third countries, Prof Fan said that was "unavoidable".

The flip side of this is that companies targeting the Chinese market may be nudged to set up base within China to avoid the tariffs, he added.

Given the complexity of modern supply chain networks, it is too early to say which country will ultimately prevail, he cautioned.

"That depends on which market is growing faster… which becomes bigger," he said. "If the China market is growing faster and becomes bigger, China may not suffer too much."

City transformed from traditional model to major hub of innovation

Four decades ago, Shenzhen was just a small fishing village adjacent to Hong Kong. Today, the city in southern Guangdong province is the country's high-tech and innovation hub.

It's known as China's Silicon Valley and is the headquarters of internet and telecom giants Tencent and Huawei, thanks to the country's reform and opening-up policy.

With a population of more than 12 million, Shenzhen's rapid growth arose from cultivating emerging industries, including the internet, new-generation information technology, new materials, new energy and biological medicine. Beyond that, energy conservation, environmental protection and the cultural and creative industries have played a key role.

Last year, the added value of emerging industries in Shenzhen amounted to about 918 billion yuan ($132 billion), increasing 13.6 percent compared with a year earlier and accounting for 40.9 percent of the city's GDP, according to official statistics.

The bioindustry saw the most robust growth, with added value expanding 24.6 percent year-on-year, followed by the internet industry at 23.4 percent.

The metropolis is now home to more than 11,000 national high-tech enterprises.

"Shenzhen's high-tech industry has already formed an integral industry chain. It has an internationalized supporting system at its back," said Huang Dinglong, chief executive of artificial intelligence company Malong Technologies.

The local government has attached great importance to research and development. Last year, Shenzhen's investment in R&D reached over 90 billion yuan, accounting for 4.13 percent of its GDP, on par with Israel and South Korea, which lead in that category.

Local policies have provided a sound breeding ground, allowing high-tech enterprises to grow in a sound environment, said Yan Qin, general manager of Direct Genomics, a company specializing in genomics.

"They don't have an extra burden, as the local government offers great support to them - for example, helping them with initial funding and understanding government policies."

In addition, with its proximity to the international financial center of Hong Kong, Shenzhen has also developed strengths in capital, with a large number of small enterprises being able to secure venture capital at early stages, Yan added.

Over the 40 years since the reform and opening-up policy was launched, Shenzhen has been an economic miracle by global standards, with its GDP growing at more than 20 percent a year on average.

In 1980, it was chosen as China's special economic zone, which entitled it to more market-oriented and flexible economic policies.

Since then, Shenzhen's economy has seen explosive expansion, from under 200 million yuan to 2.2 trillion yuan in 2017, which is more than 10,000 times bigger and on course to surpass Hong Kong.

Qu Jian, vice-president of the China Development Institute, said the city has transformed from a traditional economy reliant on resources and labor to a modern economy fueled by innovation.

"The reason so many technologically innovative enterprises have been created in Silicon Valley is that talent across the world is flocking into the area," Huang said. "It's the same for Shenzhen."

Yan, meanwhile, said local high-tech enterprises have a shortage of professional managers, who he believes play a vital role.

"Shenzhen needs to introduce more professional managers who have worked at Fortune 500 companies to improve management so that the city's high-tech industry can achieve better growth,"

XI'AN, China, Oct. 19, 2018 /PRNewswire/ -- The first Xixian New Area International Forum on Innovative Urban Development Mode (IUDM 2018), organized in Xi'an and attracting more than 500 experts and scholars from China and abroad to explore innovative urban development models, was held under the theme "New Era, New Economy, New City."

The forum was joined by Rajendra Kumar Pachauri, former chairman of the Intergovernmental Panel on Climate Change (IPCC) from 2002 to 2015; Liu Shijin, deputy director of CPPCC Committee for Economic Affairs and former vice-president of Development Research Center of the State Council; and Fan Gang, secretary-general of the China Reform Foundation and director of the National Economic Research Institute.

The IUDM 2018 placed special focus on urban development principles including city quality, living environment and applications of new technology through themed exhibitions, keynote presentations and public engagement activities. Xixian, the host district and the latest result of innovative urban development in the region, has been highlighted as a solution for future urban planning and management.

As the newest district of the greater Xi'an area, Xixian contributes to the development of urban planning through a focus on the construction of national-level free trade pilot zones, service trade zones and innovation and entrepreneurship zones as a means of boosting Shaanxi's economic growth and credentials as a hub for emerging strategic industries and services.

"Hoping to create a sample of new urbanization with Chinese characteristics, we insisted on a people-centred urban development strategy that conserves resources, preserves the environment, matches urban to rural development and protects historical and cultural heritage. Through years of tireless explorations, the result is gradually coming together," said the vice-governor of Shaanxi Province at the forum.

"Xixian New Area has entered a period of accelerated development, the IUDM 2018 forum is a new starting point, and we cordially welcome everyone to come to Shaanxi and Xixian and join us to write a magnificent new chapter of the future for urban development," said Liang.

For more information, please visit: http://en.xixianxinqu.gov.cn/

About Xixian New Area

The Xixian New Area is the first national new area themed with innovative urban development mode. It is led by innovative urban planning and city-industry integration with ecological priorities; the goal is to create a modern, sustainable city with improved ecology, livability and business environment.

SOURCE Xixian New Area

Beijing must not launch retaliatory attacks against American firms or US business operations in China, despite US President Donald Trump’s threat to slap further punitive tariffs on Chinese goods and restrict Chinese investment in the US, a Chinese economist and government adviser has warned.

“Trump would love to see [China] make trouble for US firms,” Fan Gang, a former member of the monetary policy committee of the People’s Bank of China, said in a speech at Tsinghua University in Beijing on Wednesday.

“The business community is now the only voice [in the US] that may speak for China,” Fan said. “If we target them, then we may really lose the trade war.”

Fan, a leader in an economists club founded by Vice-Premier Liu He, said that rather than focus on punitive responses to the Trump administration’s trade action, “we should further open up our market and create a fair business environment. In the long run, it’s good for China.”

Known as a liberal economist, Fan’s tone was soft in comparison with the trade war rhetoric that has come out of China’s official media since Trump began imposing punitive tariffs on Chinese goods six months ago.

But Fan’s suggestion that China focus on rolling out the red carpet for US companies and executives seemed in line with the Chinese government’s recent responses to Washington’s escalatory trade actions.

In addition to vowing to slash tariffs on US imports after Trump’s imposed punitive duties on Chinese products, Beijing has pledged to further open up its domestic market and protect the interests of foreign businesses in China, including US firms.

The government has gone the extra mile to woo foreign investment from America, granting electric car maker Tesla permission to set up an exclusively owned factory in Shanghai and giving energy giant ExxonMobil a preliminary green light to build a US$10 billion complex in Guangdong.

“The anti-China sentiment is growing in the US community, but in the past they were our alliance in the US political world,” Fan said.

The economist said China has to do some self-scrutiny and admit it has not done enough to open up its domestic market or to nurture foreign business investment.

“The American and European chambers of commerce complained about China’s business environment one year after another,” and were ignored, Fan said. “Now the US, EU and Japan are uniting their fronts, and they are not happy about China.”

China, he said, now must do many things “that should have been done in the past” to bring positive changes to its economic system and placate irritated foreign investors.

Although Fan spoke as an economist, his views also reflected a school of thought within Beijing that boldly favours China and the US reaching a compromise to reduce the intensity of the trade tensions.

“It is not just about trade imbalance,” Fan said. “In the past, we could ease the tensions by buying a few more Boeing aircraft. Not now.”

Yet, Fan also called the trade war part of a bigger plan by Washington to contain China’s rise.

“We must have long-term preparations,” Fan said. “The real intention of the US is not to reduce the trade deficit but to contain China’s development – in particular, China’s technological advancement.”

Fan said China will never sell off its US treasury holdings to hit back at the US amid the trade war because the move would hurt China more than the US. China is the single biggest foreign holder of US government debt.

“If China dumps its holdings of US treasuries, the trade war will spread to the financial realm,” Fan said. “China is vulnerable in the financial field.”

China’s holdings of US government bonds fell for a third consecutive month in August to US$1.165 trillion, down from US$1.171 trillion in July, according to the US Treasury Department.

aul Gruenwald, chief global economist at S&P Global, said in Beijing on Wednesday that the US and China may resume official talks next year in a form similar to the “Strategic and Economic Dialogue”, a now-defunct high-level communication mechanism which had helped contain divergent and often conflicting interests between the two nations through regular meetings that started in 2006.

“You have to talk, and then you can solve the problem,” Gruenwald said.

What Happened